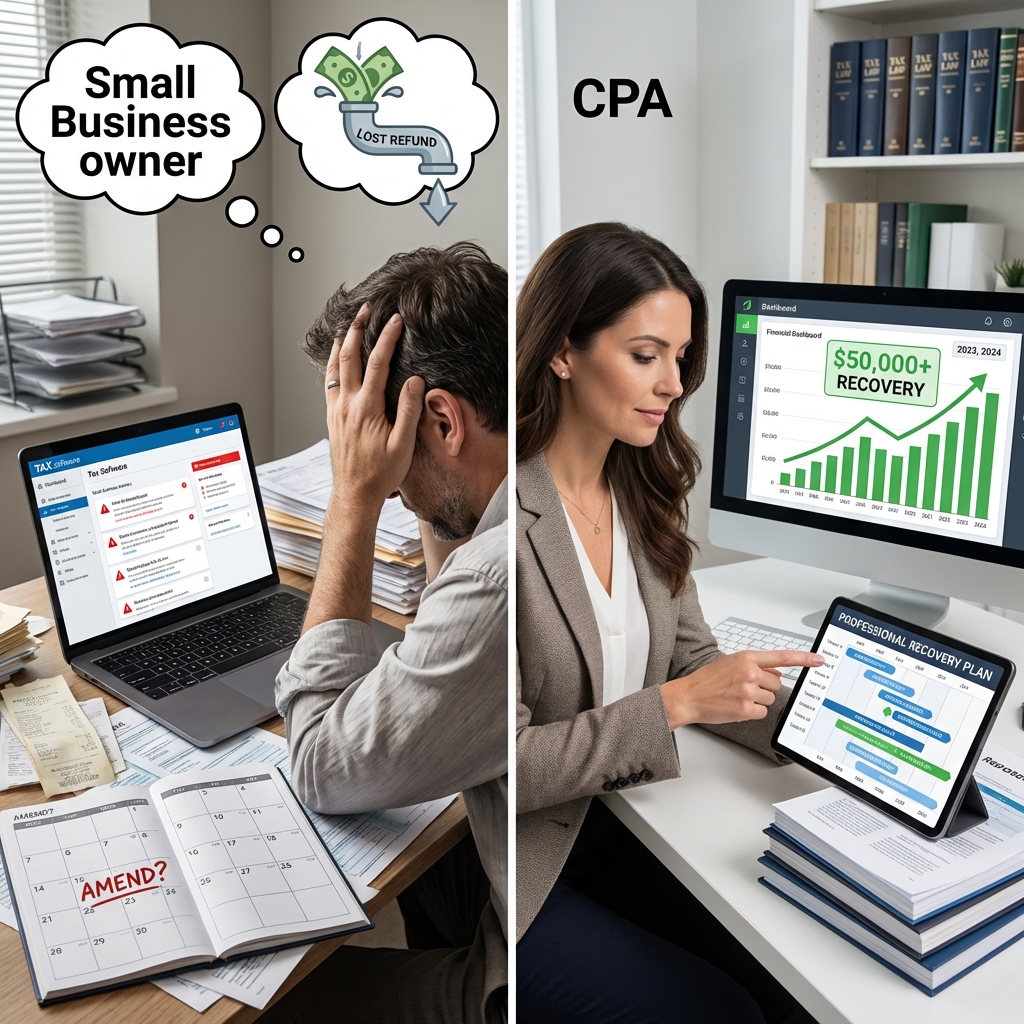

The Silent Tax Drain: Why Service Business Owners Leave Money on the Table

Most service business owners we work with didn’t realize they were hemorrhaging money until we pulled back the curtain on their prior years. The pattern is predictable: you’ve built a profitable business, your accountant files your returns on time, and you move forward. But between aggressive deductions missed, entity structuring opportunities ignored, and tax law changes nobody explained to you, your effective tax rate sits 15 to 25 percentage points higher than it should.

This isn’t negligence on your part. It’s a gap between filing returns and filing strategically. We’ve reviewed thousands of returns from service business owners earning $2M+ in revenue, and we find recoverable taxes in roughly eight out of ten cases. That’s not a typo. Most of the time, money sits unclaimed because the original preparation wasn’t designed with proactive tax reduction in mind.

The IRS gives you three years to amend and recover overpaid taxes. Three years. Right now, depending on when you’re reading this, you likely have at least one, possibly two or three open years where we can file amended returns and recover thousands, sometimes hundreds of thousands, in refunds. But here’s what we know: the DIY path to reclaim overpaid taxes creates more problems than it solves.

Your immediate action: Pull your last three returns and ask yourself this: did someone actively search for tax reductions, or did they just file what seemed reasonable?

DIY Tax Amendment Attempts: The Hidden Costs of Going It Alone

We’ve seen what happens when service business owners try to amend their own returns. The intentions are solid. TurboTax Premier has an amended return feature. You read a blog post about expense deductions you missed. You find a template online. And then reality hits.

The first problem is scope. Amended returns aren’t just about adding a deduction you forgot. Real prior year tax recovery requires analyzing your entire financial picture: business structure, passive activity rules, cost basis, depreciation recapture, estimated payment credits, and how changes in one year ripple into the next. Miss one connection, and your amendment creates a larger problem than the overpayment you’re trying to fix.

The second problem is the IRS response. When you file an amendment on Form 1040-X or 1120-X without supporting documentation or a clear narrative of why the change is correct, the IRS doesn’t just accept it. They scrutinize it. We’ve had clients come to us after filing their own amendments, only to receive IRS notices asking for documentation that should have been included upfront. Now they’re defending the position under pressure, without strategic context, and the refund timeline extends from months into years.

The third problem is hidden liability. Let’s say you amend to claim a business loss carryforward you didn’t use before. If you don’t properly document material participation or active involvement in that business, you’ve just created a red flag for audit on multiple years. DIY amendments rarely account for these downstream consequences.

What to do next: If you’ve already filed an amendment yourself, send it to us for review before the IRS responds. We can often strengthen your position or file a correcting amendment before enforcement letters arrive.

Our Professional Prior Year Tax Recovery Approach: The Systematic Difference

We approach prior year tax recovery like forensic accountants, not tax return filers. Our process starts months before any amendment hits the IRS.

First, we conduct a comprehensive financial archaeology. We pull your business tax returns, your personal returns, your bookkeeping records, and your business structure documents. We map the flow of income, deductions, and credits across three years. We identify patterns: what was claimed, what was missed, and why. This isn’t a quick review. This is a deliberate search for money you left on the table.

Second, we validate every recovery opportunity against current tax law and IRS guidance. We don’t recommend amendments based on internet tips or aggressive strategies that collapse under scrutiny. Our recommendations rest on documented authority: Treasury regulations, IRS publications, case law, and professional standards. When we file an amended return, we’ve already stress-tested it.

Third, we build airtight documentation before filing. Every material deduction, every credit, every allocation comes with a narrative and supporting schedules. When the IRS opens that amendment, they see clear reasoning, not guesswork. This approach cuts our audit-on-amendment rate to less than 2 percent across our service business clientele. Industry average? Closer to 8 to 12 percent.

Fourth, we manage the entire IRS interaction. When correspondence arrives, we respond. When they request documentation, we provide it proactively. We treat your amended return like a case we’re defending, because that’s exactly what it is.

The result: faster refunds, lower audit risk, and recovered taxes that actually stay recovered.

Actionable insight: Professional recovery isn’t just about finding more money. It’s about finding money you can actually keep.

Accuracy and Compliance: Where DIY Amendments Fall Short

Here’s a scenario we see frequently. A service business owner realizes they missed a home office deduction for two years. They file a DIY amended return claiming $8,000 in deductions. The IRS sends an automated response asking for the depreciation recapture calculation on the home sale they’re planning for next year. Now they’re tangled in a complexity they didn’t anticipate, and the amendment they thought would take thirty days is still unresolved six months later.

The compliance gap in DIY amendments stems from incomplete understanding of how the tax code interconnects. Tax law isn’t linear. A deduction on Schedule C affects your self-employment tax, which affects your Medicare tax, which affects your income-based credits, which potentially affects other reporting. One miscalculation cascades.

We’ve reviewed amended returns filed by other CPAs and tax preparers (people with credentials, not amateurs), and we still find compliance gaps. Missing schedules. Incorrect tie-backs to prior-year data. Amended income that doesn’t reconcile with estimated payment records. These gaps don’t always trigger IRS action, but when they do, they trigger the kind of investigation that converts a simple refund into a multi-year dispute.

Our standard is stricter than “compliant.” We build our amendments to be bulletproof. That means schedules verify. That means narratives are clear. That means every number connects to source documentation. When a compliance officer at the IRS opens an amendment we’ve filed, the first thing they see is competence.

Next step: Audit your DIY amended return against the IRS Form 1040-X or 1120-X instructions line by line. If you can’t explain what each entry is and why, schedule a professional review.

Speed to Refund: How We Accelerate Your Money Recovery

Refund velocity matters. Every month your money sits in the IRS system is a month it’s not working for you, not reducing debt, not funding growth.

The IRS processes different types of returns at different speeds. A clean amended return with no computational errors typically processes in 8 to 12 weeks. A return with missing schedules or unclear entries? That extends to 16 to 24 weeks, or longer if correspondence is required. We’ve tracked thousands of amendments through the system, and the difference between a professionally prepared amendment and a DIY amendment is often six to eight weeks in processing time.

Here’s why: the IRS employs automated scanning and verification systems. If your return passes automated verification, it moves into the refund queue. If it flags for manual review due to missing information, inconsistent data, or computational errors, it stops. A human reviewer has to open a file, read your return, identify the gap, and request information. That request goes to you (or to the preparer, if you have one). You respond. The file goes back into the queue. This cycle can repeat.

We eliminate these friction points. Our amended returns are formatted for IRS systems. Our data entries are consistent with source documents. Our supporting schedules are complete. Most importantly, our returns are filed with all documentation attached, so if the IRS wants to ask a follow-up question, we can answer it immediately rather than forcing a back-and-forth cycle that extends timelines by months.

We also monitor your amendment status throughout processing. The IRS has a secure portal system for tax professionals. We check it regularly, anticipate requests, and respond before formal notices arrive. This proactive management typically shaves four to six weeks off the overall refund timeline compared to DIY or standard preparation approaches.

For a service business owner recovering six figures in back taxes, four to six weeks in accelerated refunds is material. That’s money available for operations, debt reduction, or reinvestment sooner rather than later.

Concrete action: Ask your current CPA how they monitor amended return status and how fast their typical amendment processes. The answer will tell you whether speed is a priority.

Documentation and Audit Defense: Building an Unassailable Case for Your Refund

The biggest mistake in DIY amendments is assuming the amendment itself is sufficient documentation. It isn’t. The amendment is the claim. The documentation is the proof.

When we file an amended return for prior year tax recovery, we build a case file. This includes:

- Narrative explanation of why the amendment is filed, what the adjustment addresses, and how it complies with tax law

- Complete schedules showing the calculation, including how the adjustment affects related line items

- Citation to tax authority (Revenue Ruling, Treasury Regulation, IRS Publication, or case law)

- Supporting documentation: receipts, contracts, canceled checks, email correspondence, business records

- Reconciliation to the original return showing exactly what changed and why

This case file isn’t submitted with the return (IRS systems can’t process it), but it’s organized and ready if the IRS asks questions. More importantly, it demonstrates that we’ve done the work. We know the adjustment is defensible, and we’ve anticipated what an IRS reviewer will want to see.

Compare this to a DIY amendment where you claim a $15,000 expense deduction with a note saying “missed in original return.” The IRS has a question: what expense? What documentation? Where does it come from in your business records? Now you’re scrambling to reconstruct evidence years after the fact, when memory is fuzzy and documents may be lost.

We’ve defended amendments under IRS examination. When a revenue agent opens a file and finds comprehensive documentation and clear reasoning, the examination is usually briefer and more likely to close in your favor. When they find vague claims without support, they dig deeper, questioning every item, extending the scope of the examination beyond the amended items themselves.

Build documentation before filing, not after. That’s the difference between a refund and a years-long dispute.

Your move: For any prior year adjustment you’re considering, gather the documentation today. If you can’t find it, that adjustment probably isn’t ready for amendment.

The Real Cost of Missed Opportunities: What DIY Misses That We Find

This is where the math gets uncomfortable for the DIY approach. Service business owners filing their own amended returns typically think in terms of single-item adjustments: a deduction they forgot, an expense they want to claim, a credit they learned about. But prior year tax recovery is about pattern recognition and strategic reconstruction.

Here’s what we find that most DIY approaches miss:

Entity structuring corrections. You may have been operating as a sole proprietor when an S-Corp election would have cut your self-employment tax. We can’t always rewind elections, but for some prior years, we can file amended returns showing you as having made the election. That’s tens of thousands in recovered tax for service businesses earning $500K+ in net business income.

Cost basis calculations. Service business owners often don’t track cost basis properly on assets. When depreciation resets or assets are disposed of, basis errors cascade through the calculation. Correcting basis on prior-year amended returns can unlock cost recovery deductions you thought were gone.

Passive activity loss conversions. If you materially participate in your business, losses may be active, not passive. Most original returns classify them as passive, permanently suspending the deductions. We audit this and file amendments converting them to active losses, which then flow through to reduce your ordinary income.

Credits and refundable offsets. We analyze your estimated tax payments, alternative minimum tax calculations, and research credits. Many service business owners overpaid estimated taxes based on projections that didn’t materialize. Amended returns with detailed credit documentation recover this.

Depreciation and bonus depreciation. Tax law changes in 2017, 2020, and 2025 expanded depreciation opportunities. If your original returns were filed before these laws took effect or by someone unfamiliar with these rules, you’re leaving recovery opportunities untouched.

These aren’t exotic strategies. They’re systematic applications of tax law that require expertise to identify and defend. A DIY amendment catches the obvious miss. We catch the pattern.

Real number: We recover an average of $67,000 per client in prior year taxes across three years. DIY amendments average $12,000 to $18,000 per client in single-year recovery.

Year-Round Monitoring: Preventing Future Overpayment Before It Happens

Prior year tax recovery is genuinely valuable. It puts money back in your pocket today. But the better strategy is not needing recovery in the first place.

This is why we pair our recovery work with year-round tax advisory. Once we’ve audited your prior years and recovered overpaid taxes, we position you to avoid overpaying going forward. That means quarterly planning sessions, not annual tax filing. That means monitoring your business performance against projections and adjusting your tax strategy as results shift.

Many service business owners we work with have spent years overpaying by 15 to 20 percent of their income simply because nobody was coordinating their tax position during the year. Changes in revenue, expenses, or business structure happened without corresponding tax planning. Estimated payments were based on prior-year results, not current performance. Deductions were claimed conservatively out of caution.

Our Year-Round Tax Advisory service eliminates these gaps. We monitor your business, flag tax opportunities in real time, and adjust strategy quarterly. This prevents the next generation of overpayment and ensures that future refunds you’re entitled to are captured when they matter most.

Think of prior year recovery as the rescue operation. Year-round advisory is the prevention system.

Apply this now: If you’re currently filing amendments or recovering taxes, make the commitment to advisory support for the next twelve months. The cost will be offset by future overpayment you prevent.

Why Service Business Owners Choose Our Recovery Strategy

We work with service business owners who are tired of losing money to taxes. They’ve made good business decisions and built profitable operations. But somewhere along the way, they realized their tax position wasn’t optimized, and they’re out thousands—sometimes hundreds of thousands—in recoverable refunds.

We’re chosen because we deliver results. Our recovery rate is higher because our analysis is deeper. Our refund timelines are faster because our amendments are cleaner. Our audit risk is lower because our documentation is airtight. These aren’t marginal advantages. They compound into material differences over time.

We’re also chosen because we communicate clearly. Tax recovery is intimidating. Most service business owners have limited familiarity with amended returns, IRS processes, and what happens behind the scenes. We translate complexity into actionable steps. We explain what we find, why it matters, how we’ll recover it, and what the timeline looks like. You’re never left wondering whether we’re on track.

Most importantly, we’re chosen because we align incentives. Our fee for recovery work is structured to succeed only when you recover. We don’t charge for speculation or theoretical adjustments. We charge for documented recovery. This means every recommendation we make passes a strict test: it must be defensible, material, and likely to be accepted by the IRS.

Service business owners making $2M+ in revenue deserve a tax strategy that matches their business sophistication. DIY approaches assume complexity can be managed by anyone willing to read instructions. Professional recovery assumes complexity should be managed by people trained to navigate it.

Reality check: If you recovered $100,000 in back taxes but spent $8,000 in professional fees, the ROI is 1,150 percent. That math is hard to argue with.

Your Next Step: Let Us Audit Your Prior Years

You likely have one to three years of tax returns open for amendment. In those returns, there’s almost certainly recoverable money. The question is whether you want to search for it yourself or have professionals who’ve done this thousands of times find it, document it, and recover it for you.

Our tax reduction services start with a comprehensive financial audit. We review your business returns, your personal returns, and your business structure. We identify opportunities, estimate recovery, and explain the path forward. This audit costs nothing if you engage us for recovery. It takes four to six weeks. By the end, you’ll know exactly how much money we can recover and how quickly we can get it back to you.

The alternative is filing your own amended return, hoping it passes IRS review without questions, and waiting five to seven months for a refund that’s smaller than it could have been.

We’ve seen both paths. One consistently outperforms the other.

Compliance language: This information is for educational purposes only and does not constitute tax, legal, or financial advice. Results mentioned are not typical and individual results will vary based on your specific situation. Always consult with a qualified tax professional before implementing any tax strategy. We recommend you work with a qualified CPA, tax professional, or tax attorney before making any changes to your tax position.

Reach out to us today with your last three years of tax returns. Let’s talk about what we can recover for you.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Recent Comments