The Tax Planning Crisis for High-Income Service Business Owners

You’re making excellent money. Your service business hit $2M+ in revenue. You’re profitable, disciplined, and reinvesting back into growth. Then tax day arrives and the reality hits: you’re writing a check to Uncle Sam that makes your stomach turn.

This isn’t an anomaly. We work with service-based business owners every single week who are genuinely shocked by what they owe. A consultant clearing $750K in taxable income. An agency owner with $2.5M revenue paying an effective tax rate that rivals a small country. A boutique firm founder realizing they’ll owe $400K+ when they thought they’d have breathing room.

The painful truth: most high-income service business owners are trapped in a tax planning gap. They have enough complexity to warrant serious strategy, but not enough sophistication in their current advisory setup to capture the opportunities. Traditional CPAs handle compliance. Tax coaches offer education. But few deliver what you actually need: coordinated, proactive, dollar-specific tax reduction tied directly to your business operations.

This gap costs service business owners hundreds of thousands annually in preventable taxes.

Why Traditional Tax Approaches Leave Money on the Table

Let’s pull back the curtain on how conventional tax planning fails high-income service businesses.

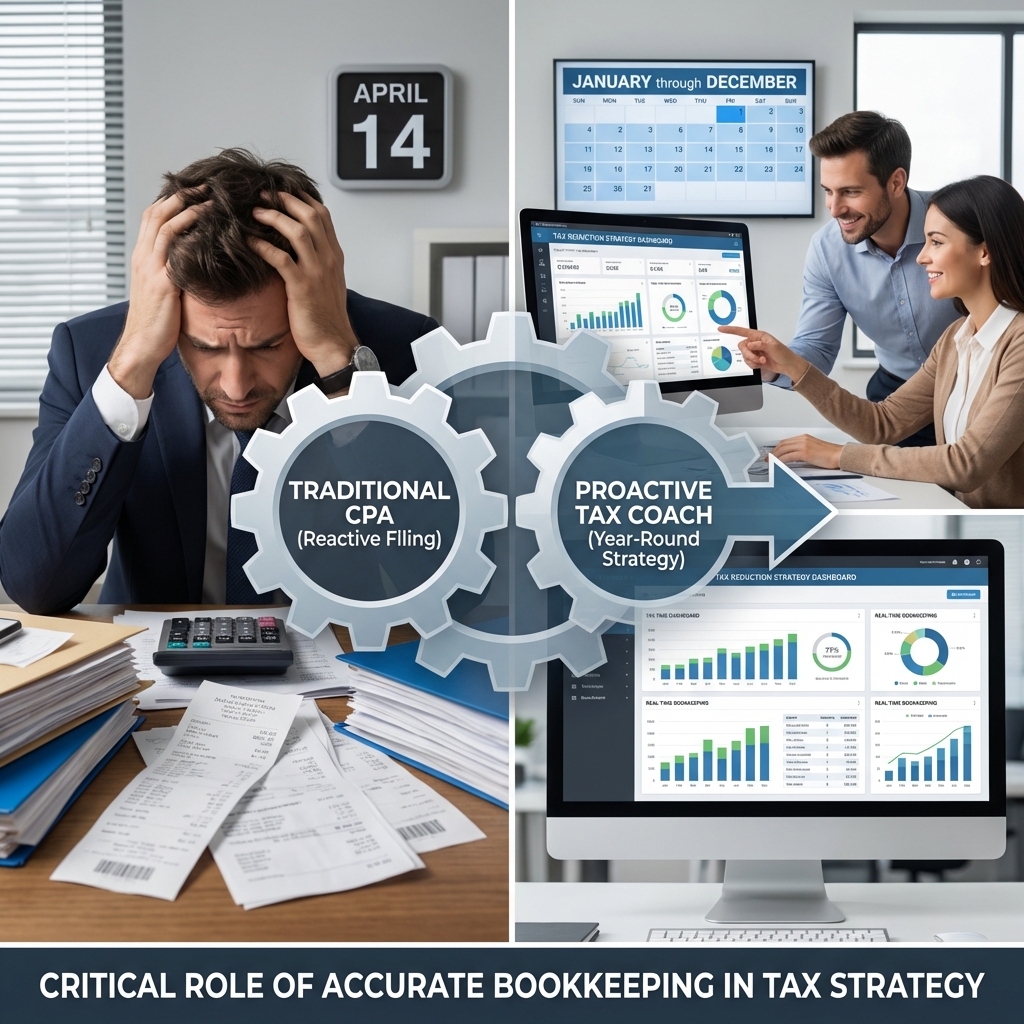

The compliance-only CPA model works great for straightforward W-2 earners. File the return, claim standard deductions, done. But for you? It’s leaving mountains of strategy on the table. Your CPA processes what happened last year. They don’t reshape what happens this year or next.

Meanwhile, the education-first tax coach model teaches principles brilliantly but stops short of coordinated execution. You learn about entity structure, passive loss conversion, and the 100-Hour Test. You understand the concepts. But implementation requires real-time bookkeeping accuracy, ongoing tax modeling, and business decision coordination that solo education can’t deliver.

Here’s what gets missed most often:

- Passive loss conversion opportunities buried in your current structure

- Real estate and equipment strategy never properly quantified or coordinated with operations

- Year-round cash flow and estimated tax management that prevents the April surprise

- Timing of income recognition and expense deductions misaligned with your actual tax liability

- Business decisions made without modeling their tax impact first

You don’t need generic tax education. You need someone inside your business, tracking it continuously, and turning insights into action before the tax bill arrives.

Understanding Different Tax Advisory Models

The market offers roughly three flavors of tax guidance, and understanding the differences matters.

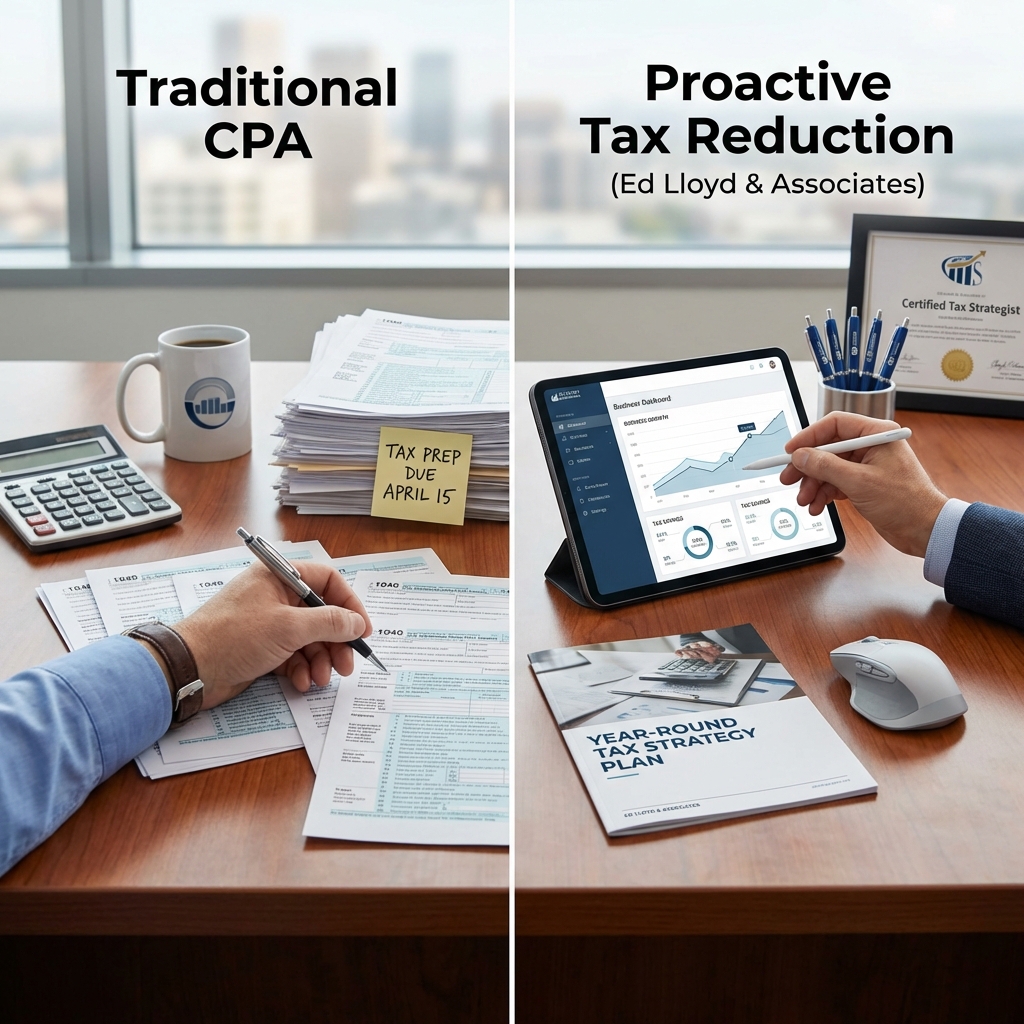

The Traditional CPA: Files your return after year-end, itemizes deductions, and maybe identifies one or two obvious strategies. Reactive, compliance-focused, limited advisory depth. Cost: typically $2K-$8K annually for your complexity level. Value: legal coverage and accurate filing. Limitation: zero proactivity.

The Tax Coach or Remote Tax Strategist: Teaches frameworks, sells courses or memberships, offers group coaching, and positions you as the implementer. Excellent for education. Cost: $500-$3K yearly or one-time course fees. Value: conceptual clarity and principles. Limitation: no ongoing business integration, no execution oversight, no accountability for actual results.

The Integrated Tax Strategy Firm: Combines compliance, ongoing bookkeeping, continuous tax modeling, strategic advisory, and real-time decision support. Knows your books intimately. Models changes before you make them. Adjusts strategy quarterly based on actual performance. Cost: typically $8K-$25K+ annually depending on complexity and revenue. Value: integrated strategy execution, proactive reduction, documented results, ongoing optimization.

Most service business owners compare models 1 and 2 because they’re cheaper upfront. But if you’re paying $200K+ in avoidable taxes annually, the cheapest model isn’t the one that costs less per hour. It’s the one that delivers more dollars back to you.

Our Proactive Tax Reduction Philosophy at Ed Lloyd & Associates

We operate from a fundamentally different premise than traditional CPA firms.

You don’t need better compliance. You need better tax reduction. We design every engagement around one outcome: keeping more of what you earn through coordinated, legal, documented strategy.

Our philosophy rests on three pillars:

- Continuous Visibility: We maintain current books and financial data throughout the year, not just at filing deadline. This lets us model scenarios in real-time, not post-mortems.

- Proactive Modeling: Before you make a major business decision (hiring, equipment purchase, bonus structure, loan payoff), we model its tax impact. You decide with full visibility.

- Documented Strategy: Every recommendation is tied to specific tax law, quantified by dollar impact, and tracked for audit defensibility. We don’t suggest tactics. We execute strategies.

Our goal isn’t to be your cheapest advisor. It’s to be the advisor who saves you the most money after fees. We work primarily with service-based business owners earning $500K+ in taxable income because the math is clear: at that income level, even a 5% tax reduction saves $25K+. That justifies sophisticated, integrated advisory.

We’ve helped our clients reduce income taxes by 50% or more. Results mentioned are not typical and individual results will vary based on your specific situation. But when you’re in the target zone—profitable service business, complex income streams, actively seeking strategy—material reductions are realistic and repeatable.

Year-Round Tax Planning vs Once-a-Year Tax Prep

The calendar year creates a false deadline that drives terrible tax decisions.

Most businesses think tax planning happens in December. Maybe January if they’re early. Then they scramble: “What can we do before year-end?” Equipment deductions. Retirement contributions. Bonus strategies. Whatever fits through the closing window.

This backwards approach leaves 11 months of planning potential on the table.

We operate on continuous quarterly planning cycles. Q1 finishes: we have actual numbers. We model full-year projections, identify tax exposure, and recommend actions for Q2-Q4. Q2 adjustments arrive as new information hits. By Q4, there are no surprises because we’ve been optimizing continuously.

Real example: A consulting firm owner projected $650K taxable income in November. Standard response: “Throw money at retirement or equipment.” Our response: model what happens with a strategic S-corp election, restructure their 1099 contractor base, and adjust their wage/distribution mix. Result: $185K reduction in federal income tax that year. But only because we had continuous visibility. A year-end prep firm would’ve suggested the same generic tactics as everyone else.

The difference between once-a-year prep and year-round planning isn’t efficiency. It’s leverage. More data points, more strategy windows, more precision.

The Critical Role of Bookkeeping in Tax Strategy Execution

You can’t execute tax strategy on sloppy books.

This is where many advisory relationships fail silently. A great tax strategist recommends converting passive losses to active. Brilliant concept. But your bookkeeper doesn’t understand material participation rules. They code the rental property expense to the wrong account. Your documentation gets muddied. The strategy either doesn’t work or invites audit risk.

We handle both bookkeeping and tax strategy under one roof, for one reason: they’re not separate functions. They’re linked operations.

Our bookkeeping isn’t basic data entry. It’s strategy-first accounting. We code transactions with tax strategy in mind. We maintain documentation for every strategic decision. We track metrics (material participation hours, related-party transactions, qualified business income flows) that matter for tax planning, not just revenue reporting.

When you use an external bookkeeper and a separate tax advisor, they’re making assumptions about each other’s work. When we own both, every journal entry supports your tax position.

Action takeaway: Audit your current bookkeeping practices. Ask your bookkeeper: “Do you understand the tax strategies we’re trying to execute?” If the answer is hesitation or vagueness, there’s a coordination gap costing you money.

Advanced Tax Strategies We Implement for Our Clients

Let’s get tactical. These aren’t theoretical tax hacks. These are concrete strategies we’re actively deploying for service business owners in 2026.

S-Corp Wage Optimization: Service businesses often report all income as self-employment. But S-corp structure lets you split income into reasonable W-2 wages and distributions, cutting self-employment tax significantly. The IRS expects “reasonable” compensation (they’ll challenge low wages), but within that band, the savings are substantial. A $500K net income consulting business might shift $300K to wages and take $200K as distributions, cutting self-employment tax by $6K-$12K annually.

Qualified Business Income (QBI) Positioning: The 20% deduction under Section 199A is still widely underutilized. But service businesses (consulting, agencies, professional services) face wage/property limitations that reduce QBI benefits. We structure entities and track metrics to maximize available QBI while staying IRS-compliant.

Real Estate and Equipment Strategy: Service owners often ignore depreciation opportunity. A $100K equipment purchase can generate $20K+ in deductions through accelerated depreciation. Layered with bonus depreciation rules, this front-loads deductions into high-income years. But only if you buy strategically and document properly.

Passive Loss Conversion: If you own rental real estate or passive investments, losses can shelter other income. Material participation rules let you convert passive losses to active losses, unlocking deductions that would otherwise carry forward indefinitely. The 100-Hour Test and other material participation tests are your gateway, but they require real-time tracking and intentional business conduct.

Retirement Contribution Stacking: Solo 401(k)s, defined benefit plans, and SEP-IRAs aren’t new. But their interaction with your payroll structure, S-corp status, and income levels matters enormously. We model contribution limits annually and often unlock $20K-$50K+ in additional deductions service owners didn’t know were available.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy.

How We Identify Hidden Tax Savings Most CPAs Miss

Standard tax software follows a formula: take gross income, apply standard deductions, compute liability. It catches obvious opportunities (mortgage interest, charitable donations) but misses structural optimization.

We approach tax planning differently. We start with your specific situation:

- Income Composition Analysis: Where does your money actually come from? W-2 wages, 1099 income, passive distributions, capital gains? Each source has different tax characteristics. Service businesses mixing income streams have untapped optimization potential.

- Entity Structure Audit: Are you in the right structure for your situation? An S-corp isn’t always better than an LLC taxed as a sole proprietor. A partnership might be superior to both. We model the numbers, not follow convention.

- Deduction Completeness Review: Beyond standard business expenses, are you capturing home office deductions, vehicle mileage, education, travel, and equipment properly? Many service owners under-deduct due to outdated guidance or fear of audit.

- Retirement Plan Optimization: If you’re self-employed or have employees, are you maximizing available retirement contribution space? A solo 401(k) can shelter $70K+ annually depending on income. Most service business owners leave this untapped.

- Related-Party Transaction Review: Do you buy services from family members or related entities? Rent from properties you own? Pay yourself distributions? These create planning opportunities many advisors avoid due to audit sensitivity, but properly documented, they’re powerful.

The difference between a standard CPA and our approach: they process what you give them. We reverse-engineer what your situation allows.

The Real Cost of Delaying Proactive Tax Planning

Procrastination on tax strategy has a compound cost that most service business owners underestimate.

You earn $600K in taxable income this year. You delay strategy, so you pay full freight: maybe $180K-$210K in federal income tax depending on state. Next year, same delay, same cost. Three years of delay costs you roughly $600K in preventable taxes, assuming 10% reduction potential is realistic.

But it’s worse than that. Strategy compounds. A retirement plan established this year grows tax-free for 20+ years. A business structure optimization this year saves not just this year’s taxes, but every subsequent year. A real estate strategy started now positions you for decades of deductions. Delay means you never capture those years.

Here’s the actual math many service owners face: Starting aggressive tax planning at $500K income saves roughly $25K-$50K annually (conservative estimate). If you delay two years, you’ve already forfeited $50K-$100K. By the time you engage us, you’re trying to catch up on missed years that can’t be recovered without amendment filings (which have their own costs and limitations).

The urgency isn’t pressure sales. It’s basic math: every year you delay is another year of taxes paid that strategy could’ve prevented.

Taking Action: Your Next Steps to Keep More of What You Earn

If you’re reading this, you’ve probably felt the frustration of overpaying taxes despite professional advice.

Here’s what we recommend immediately:

Step 1: Assess your current advisory setup. Are you getting proactive tax reduction, or compliance only? Ask your current advisor this directly: “What’s your specific plan to reduce my tax bill this year, and by how much?” Their answer tells you everything.

Step 2: Model your current trajectory. Work with a tax professional to project your full-year taxes based on current run rate. Don’t wait for April shock. Know the number now.

Step 3: Connect with us for a strategy consultation. We specialize in service-based business owners earning $500K+ in taxable income. We’ll review your current situation, identify 2-3 specific opportunities we see immediately, and quantify potential savings. No fluff, just specific numbers.

We’ve built CPA tax reduction services specifically for business owners frustrated by overpaying. We pull back the curtain on what’s possible, and then we execute it. Our clients reduce income taxes by 50% or more—results mentioned are not typical and individual results will vary based on your specific situation—but only because we coordinate strategy, bookkeeping, and decision-making continuously.

The gap between what you’re currently paying and what you could legally pay is real. The question is whether you’ll close it this year or keep leaving money on the table.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Recent Comments