Table of Contents

- The Hidden Tax Trap Most Founders Miss Before Selling

- Why Standard Tax Prep Won't Protect Your Exit

- The Three Critical Areas We Audit Before Your Sale

- Entity Structure: Did You Set This Up for an Exit?

- Expense Documentation: The IRS Loves to Challenge Sellers

- Passive Loss Carryforwards: Your Hidden Tax Time Bomb

- The Real Cost of Skipping Pre-Sale Tax Cleanup

- How Our Proactive Audit Process Protects Your Deal

- The Cleanup Timeline That Matters Before Closing

- Your Tax Position Is Your Negotiating Position

- Moving Forward: Your Pre-Sale Action Plan

- Frequently Asked Questions (FAQ)

The Hidden Tax Trap Most Founders Miss Before Selling

You’re close to the finish line. Your service business has scaled to millions in revenue, you’ve built something real, and now you’re staring down a potential exit. But before you sign that purchase agreement, one critical question looms: Are you about to leave millions on the table because of tax liabilities the buyer’s due diligence team will uncover?

We’ve seen it happen too many times. Founders negotiate hard on valuation, only to watch half their gain evaporate when tax surprises surface during underwriting. The difference between a smooth exit and a painful one often comes down to whether you pulled back the curtain on your tax position before the buyer did.

This is where a pre-sale tax audit becomes your most valuable negotiating asset.

Most founders assume their annual tax returns are sufficient preparation for a sale. They’re not. Your CPA files your return on April 15th each year, but they’re not thinking about transaction tax liability, audit risk, or structural implications that only surface during buyer due diligence.

Here’s the trap: the IRS doesn’t care that you’re selling. They see accumulated passive losses, deductions that weren’t properly documented, entity structure decisions made in year two that now expose you to double taxation, and missing substantiation for years of claimed business expenses. Buyers see these issues too, and they’ll demand either a reduction in price or escrow holdbacks to cover potential exposure.

One founder we worked with was selling his consulting firm for $8 million. During our pre-sale audit, we uncovered $340,000 in passive loss carryforwards that were never converted to active losses due to a structural oversight. The buyer’s tax counsel flagged it immediately. That founder either had to accept a seven-figure reduction in proceeds or restructure the deal to shield that liability. We helped him restructure, but he could have avoided the pressure entirely with a proper audit beforehand.

Your next step: Stop assuming your tax filings are audit-proof. Treat them as a starting point, not a completion.

Why Standard Tax Prep Won’t Protect Your Exit

Tax preparation is backward-looking. Your tax professional gathers documents from last year, calculates your liability, and files your return. That’s their job, and it’s important. But it’s not forward-looking, and it’s not transaction-focused.

When you’re selling, you need something different: a forensic review of your tax position from a buyer’s perspective. What deductions will they challenge? What documentation gaps exist? Which accounting positions could trigger an audit or create deal friction? A standard tax prep engagement doesn’t include that lens.

Consider a common scenario: you’ve been claiming home office deductions for eight years with minimal documentation beyond a rough square-footage calculation. Your CPA includes it on your Schedule C, and you pay taxes accordingly. But when a buyer’s accountant reviews your files during due diligence, they see red flags. The IRS has been aggressive on home office deductions for self-employed service providers. The buyer now wants proof of legitimate business use, and if you can’t provide it, they’re demanding either repayment of those deductions in the purchase agreement or a price reduction.

We approach it differently. During a pre-sale tax audit, we simulate the buyer’s scrutiny. We review your documentation. We identify gaps. We estimate potential exposure. Then we help you remediate before you’re in a weakened negotiating position.

Your takeaway: Transaction-focused tax planning requires a different skill set than annual tax filing. One doesn’t replace the other.

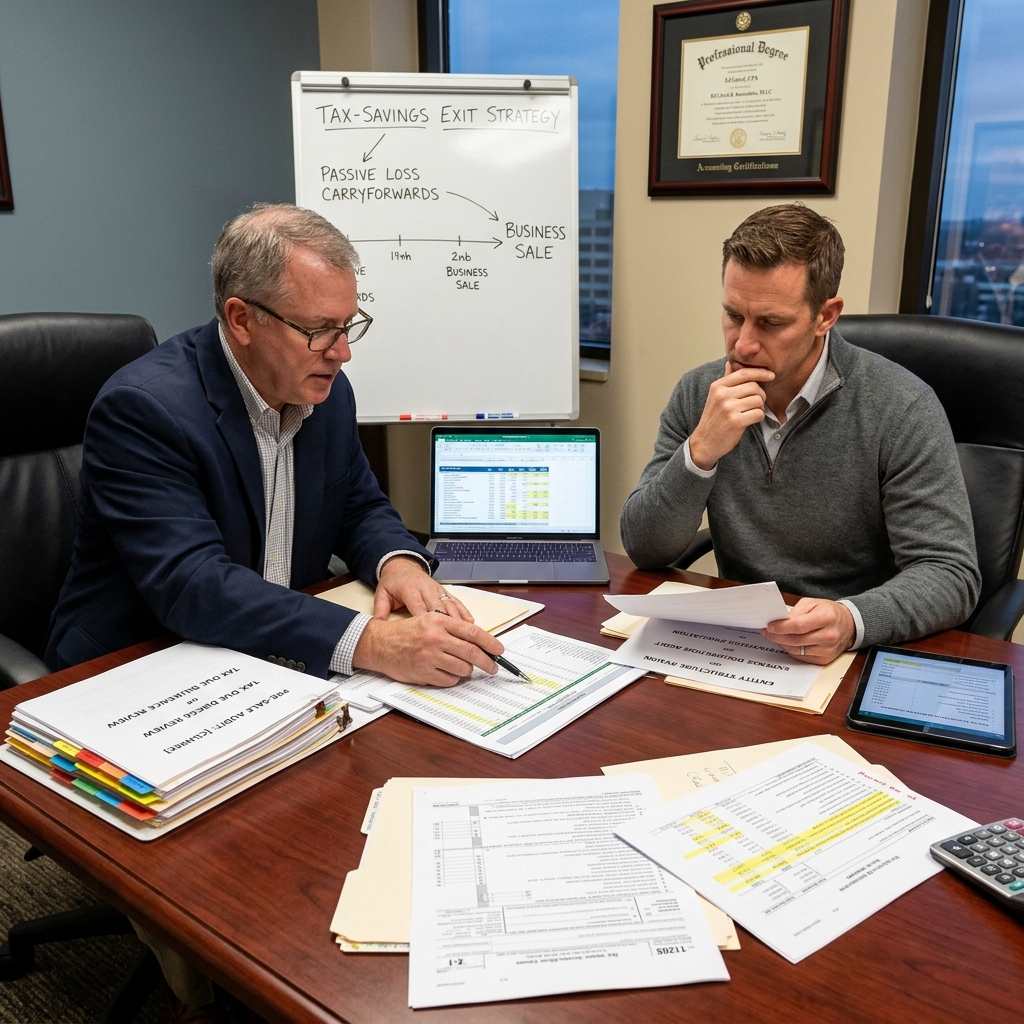

The Three Critical Areas We Audit Before Your Sale

When we conduct a pre-sale tax audit, we focus on three interconnected areas that consistently create deal friction and tax liability for service business owners.

First, entity structure and jurisdiction decisions. Did you form as an S-corp, C-corp, or LLC? Did you make a late Section election that triggered unexpected corporate-level tax? Are you selling shares (capital gain) or assets (different tax treatment on deductions)? These questions determine your tax bill and the buyer’s post-closing liability, and they can’t be changed retroactively once the deal closes.

Second, expense documentation and substantiation. We review five to seven years of claimed deductions and assess audit risk. Travel expenses, meals, auto expenses, contract labor, and equipment purchases all face IRS scrutiny when a business sells. We want to know which ones you can defend and which ones look weak.

Third, passive loss carryforwards and suspended deductions. Many service business owners have accumulated losses from prior years that they’ve been unable to deduct because they don’t meet material participation thresholds or because they’re passive activities. These become critical during a sale because the buyer inherits the risk, and you may be able to unlock deductions you didn’t realize were still sitting on your books.

This three-part framework helps us build a clear picture of your tax position before the buyer’s due diligence team does.

Entity Structure: Did You Set This Up for an Exit?

Your business entity structure was likely chosen based on liability protection and annual tax burden when you formed it. But when you sell, it becomes one of the largest tax variables in your transaction.

If you operate as an S-corp and the buyer wants to buy your company’s assets (not shares), you face pass-through taxation plus a potential corporate-level tax hit when you liquidate the company. If you’re structured as an LLC taxed as a C-corp, you’re already dealing with double taxation on dividends, and a sale compounds that.

We’ve also seen founders who made late or unsuccessful Section 1362 elections years ago that created hidden tax exposure. We audit your entity structure decisions against your sale strategy to identify friction before underwriting begins.

The fix often comes down to proactive restructuring months before your sale closes. Sometimes it’s worth reorganizing into a cleaner entity structure if it saves six figures in transaction taxes. Sometimes it means documenting why your current structure is actually optimal given your buyer’s deal structure. Either way, you want this clarity now, not during closing.

Action item: Pull your corporate formation documents and last five years of tax returns. Verify that your entity elections align with your exit strategy.

Expense Documentation: The IRS Loves to Challenge Sellers

Service businesses operate with lower capital requirements than product-based businesses, which means your deductions matter. You’ve claimed thousands in home office, vehicle, meals, travel, and contract labor expenses over the years. But can you prove them?

Buyers and their accountants know the IRS scrutinizes these categories heavily. If your documentation is thin, they’ll demand an escrow holdback or price concession to account for potential audit exposure they inherit.

We conduct a granular review of your largest expense categories. Here’s what we look for:

- Vehicle expenses: Miles logged, business purpose documented, personal use separated. Vague “business use” won’t survive buyer scrutiny.

- Meals and entertainment: 50% deductible (post-2025), but you need contemporaneous notes on who, why, and business purpose.

- Contract labor: 1099s issued, substantiation of work performed, verification that workers actually existed and performed services.

- Travel: Destination, dates, business purpose, attendees. Generic “conference trip” expense entries are red flags.

- Home office: Square footage calculations, rent allocation, utilities, insurance properly apportioned.

For each category, we estimate the IRS audit risk and potential disallowance. If the risk is material, we work with you to either strengthen documentation or prepare a detailed memo explaining the business rationale.

Your action here: Gather five years of expense summaries by category. Identify your three largest deduction categories and assess how defensible they are with your current documentation.

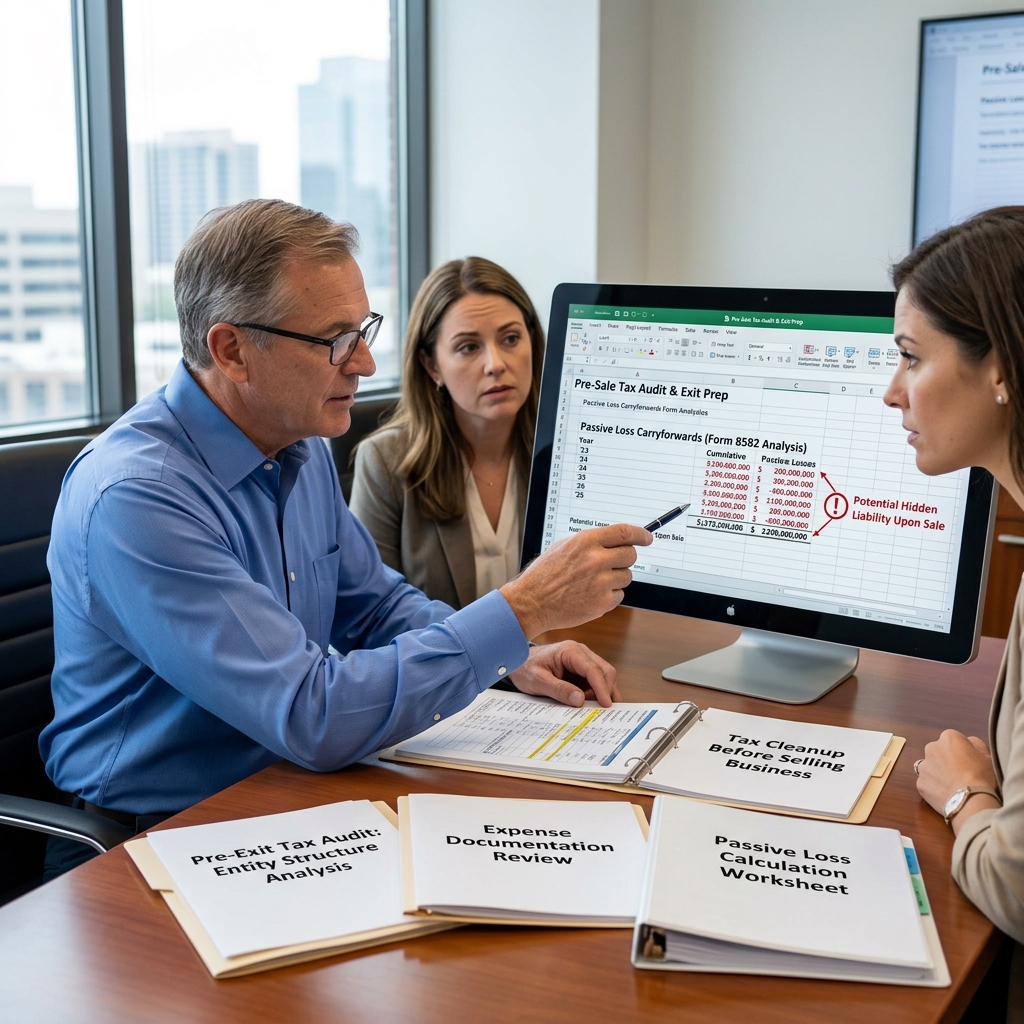

Passive Loss Carryforwards: Your Hidden Tax Time Bomb

This is the one most founders miss entirely until it explodes during a sale.

If you have investments in rental properties, partnerships, or other passive activities, you may have accumulated passive losses over years that you couldn’t deduct because you didn’t meet material participation thresholds. Under tax law, these losses get suspended and carried forward indefinitely. But here’s the trap: they create a massive issue during a sale.

When you sell your business and trigger a seven-figure gain, the buyer’s tax counsel will ask about your overall tax position. If you have $200,000 in suspended passive losses sitting on your books, they become relevant. In some situations, a business sale can trigger disposition events that unlock these losses. But more often, they remain suspended, and the buyer wants to understand why their acquisition creates this contingent liability.

We audit your passive activities, identify all suspended losses, and determine whether your sale structure can unlock any of them. Sometimes we can restructure the transaction to convert passive losses into active losses, which saves you material tax dollars.

One founder had invested in a rental property partnership years ago that generated annual losses he couldn’t deduct. By the time he sold his service business, he had $180,000 in suspended losses. We restructured his exit to classify those losses as active losses available in the transaction year. That moved the needle by roughly $45,000 in his after-tax proceeds.

Critical step: Request a statement from any partnerships, S-corps, or rental properties you invest in showing your suspended loss balances. Bring that information into your pre-sale audit.

The Real Cost of Skipping Pre-Sale Tax Cleanup

Scenario: You skip the pre-sale audit because it feels like an extra cost and an extra timeline burden. You get a letter of intent from a buyer at your target valuation. You’re excited.

Then the buyer’s due diligence team requests tax details. They ask for documentary support on major deductions. They flag passive loss carryforwards. They question your entity structure tax treatment. Your deal team now has to negotiate tax representations and indemnities in the purchase agreement. The buyer demands an escrow holdback to cover potential tax exposure. Your deal takes three months longer to close, and you end up signing a purchase agreement that reduces your proceeds by $400,000 because of tax uncertainties that surfaced during underwriting.

Alternatively, you conduct a pre-sale tax audit three months before you go to market. We identify the same issues, but now you control the narrative. You can remediate documentation gaps. You can restructure if needed. You can build a clean tax picture and disclose it proactively in your financial materials. Buyers see a founder who’s thought through their tax position, which increases deal confidence and reduces friction.

The difference between those two scenarios: six figures in proceeds and deal timeline certainty.

The math is simple: A $10,000 pre-sale audit is insurance against a potential $300,000+ loss of deal value or deal timeline slippage.

How Our Proactive Audit Process Protects Your Deal

We start with a detailed intake focused specifically on your sale timeline and buyer expectations. We’re not preparing your 2026 tax return; we’re auditing your tax position from a transaction perspective.

Here’s our process:

Month One: Forensic Review. We analyze five to seven years of returns, document your entity structure, map passive activities, and conduct a granular review of your largest deductions. We’re building a complete picture of your tax exposure.

Month Two: Gap Identification and Remediation Planning. We identify documentation gaps, entity structure issues, and passive loss opportunities. For each material finding, we develop a remediation plan with timeline, cost, and expected impact on your deal.

Month Three: Buyer Readiness. We prepare a detailed tax summary and disclosure statement for your deal team. We identify any remaining tax risks and build a representation and indemnity strategy to minimize escrow holdbacks or price concessions.

We also serve as a tax advisor during your buyer conversations, helping your deal team understand tax-related pushback and negotiate reasonable positions.

This is what pre-sale tax planning actually looks like when you’re serious about protecting your exit. It’s not a one-time calculation; it’s a strategic engagement designed to maximize your after-tax proceeds and minimize deal friction.

The Cleanup Timeline That Matters Before Closing

Timing is critical. Start your pre-sale tax audit at least four to six months before you expect to go to market with your business.

Why? Some remediations require time. If we identify documentation gaps on major deductions, we may need to reconstruct records or prepare detailed business justification memos. If we recommend entity restructuring, that requires time to execute and test the tax position. If we identify passive losses to unlock, we need to plan the transaction structure carefully.

A compressed timeline pushes you into reactive mode. You’ll make decisions under pressure instead of strategic clarity.

Ideal timeline:

- Months -6 to -5: Initiate pre-sale tax audit. Identify issues.

- Months -5 to -4: Execute remediations and restructuring if needed.

- Months -4 to -3: Prepare tax disclosures and buyer materials.

- Months -3 to 0: Go to market and field offers. You now have a clean tax picture.

If you’re already at the letter of intent stage, it’s not too late. We can still conduct a post-LOI tax review and help negotiate tax-related terms. But you’ll be negotiating from weakness instead of strength.

Your deadline: Initiate a pre-sale tax audit now if you expect any exit activity in the next 18 months.

Your Tax Position Is Your Negotiating Position

Here’s the provocative truth: your tax position directly impacts your deal valuation and closing certainty.

Buyers understand that acquiring a business means inheriting its tax liabilities. If you have undocumented deductions, suspended losses, entity structure complexity, or audit risk, they’ll price that in. They’ll demand representation and indemnity insurance. They’ll push for escrow holdbacks. They’ll take longer to close while they assess risk.

But if you’ve already pulled back the curtain on your tax position and demonstrated that you’ve thought it through, that you’ve remediated issues, and that your tax picture is clean and defensible, you’re negotiating from a position of confidence. You’re a founder who’s serious about the sale and who’s protected their buyer’s interests.

That confidence translates to faster deals, higher valuations, and better closing certainty.

We’ve seen deals where a founder’s willingness to invest in a pre-sale tax audit literally accelerated closing by two months and protected seven figures in deal value. Because the buyer didn’t have to spend underwriting time and money auditing tax risk; the founder had already done that work.

Think about it: Your buyer would spend $50,000 to $100,000 on their own tax due diligence if you don’t. Wouldn’t you rather control that narrative yourself?

Moving Forward: Your Pre-Sale Action Plan

You don’t have to navigate this alone. This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

Here’s what we recommend as your next step:

Step One: Gather your last three years of tax returns, entity formation documents, and a summary of your largest deductions by category.

Step Two: Schedule a 30-minute conversation with our team. We’ll ask questions about your sale timeline, your expected buyer type, and your exit goals. We’re not selling you anything in this conversation; we’re understanding your situation.

Step Three: We’ll provide a preliminary assessment of the most likely tax issues we’d surface in a full audit, along with a timeline and investment for a complete pre-sale tax audit.

If you’re serious about keeping more of what you earn when you exit, a pre-sale tax audit is the single most important investment you can make right now. You’ve spent years building this business. Don’t leave millions on the table because of tax uncertainties that could have been identified and addressed months before closing.

The clock is ticking. Reach out today.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

What makes a pre-sale tax audit different from our standard tax preparation?

We focus our pre-sale audits on identifying tax liabilities and missed deductions that standard tax prep overlooks, because selling triggers completely different IRS scrutiny than running your business does. Our audit examines your entity structure, expense documentation, and passive loss carryforwards specifically through the lens of what a buyer’s accountant and the IRS will scrutinize. We’re essentially pulling back the curtain on your tax position before it becomes a negotiating weapon against you.

How much time do we need before closing to handle tax cleanup?

The timeline depends on what we uncover, but we typically recommend starting our audit process 6-9 months before your target close date. Some issues like passive loss restructuring or expense substantiation require time to document and potentially file amended returns. We’ll give you a clear cleanup roadmap after our initial audit so you know exactly what we can resolve and which items need advance planning.

Can we still do meaningful tax cleanup if we’re already in active sale negotiations?

We can work with compressed timelines, but your negotiating position weakens substantially once a buyer knows about unresolved tax exposure. This is why we push founders to handle cleanup proactively before the sale process begins. Even if you’re already in talks, we can often negotiate extended closing periods or holdback structures that protect you from post-sale tax surprises we could have prevented earlier.

Recent Comments