Table of Contents

- The $800K Taxable Income Problem: Why You're Leaving Money on the Table

- Understanding Self-Employment and Payroll Tax Burden

- Entity Structure Decisions That Cut Your Tax Bill

- S-Corp Election Strategy for Maximum Savings

- Qualified Business Income Deduction Optimization

- Expense Categorization and Deduction Maximization

- Timing Strategies for Estimated Tax Payments

- Building Your Year-Round Tax Advisory Foundation

- Common Mistakes High-Income Service Owners Make

- Taking Action: Your Path to Significant Tax Reduction

- Frequently Asked Questions (FAQ)

The $800K Taxable Income Problem: Why You’re Leaving Money on the Table

You’re running a service business. Revenue is strong. Profits are solid. But when April arrives, you’re writing a check that makes your stomach turn.

This is the hidden tax trap most high-income service owners never see coming. If you’re earning $800K in taxable income, self-employment tax alone can cost you $113,000 or more annually. That’s not income tax. That’s just the 15.3% combined Social Security and Medicare tax on net earnings from self-employment.

We’ve worked with hundreds of service-based business owners in this exact situation. Consultants, contractors, therapists, coaches, and digital agencies pulling substantial revenue but paying what feels like a penalty for success. The frustrating part? Most of that burden is avoidable through deliberate strategy.

The difference between owners who understand tax structure and those who don’t is routinely $50K to $150K per year in savings. This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy.

Your action here is simple: stop assuming your current structure is permanent. It’s not.

Understanding Self-Employment and Payroll Tax Burden

Self-employment tax is the enemy of service business owners. Unlike W-2 employees who split payroll taxes with their employer, you pay the full 15.3% solo. That includes 12.4% for Social Security (capped at $168,600 of income in 2026) and 2.9% Medicare (no cap).

Do the math on a $400K net profit from your service business: you’ll owe roughly $56,800 in self-employment tax before you even consider federal and state income tax. That money vanishes.

Here’s where payroll tax reduction strategies become critical. The right entity structure and compensation strategy can convert a portion of that self-employment income into W-2 wages, where you split the tax burden with your business. On paper that seems neutral, but the actual mechanics create real savings through deduction opportunities and income shifting.

The key insight: not all business income is created equal for tax purposes. Some can be sheltered. Some can be deferred. Some can be paid as reasonable W-2 wages instead of self-employment income.

Your immediate takeaway: if you’re currently a sole proprietor or single-member LLC taxed as a sole proprietor, you’re likely overpaying by thousands every quarter. This structure works fine at $200K revenue. It becomes a liability at $800K.

Entity Structure Decisions That Cut Your Tax Bill

Your business entity is the foundation of every tax strategy that follows. The wrong structure locks you into higher taxes no matter what else you do.

We typically guide high-income service owners toward one of three structures:

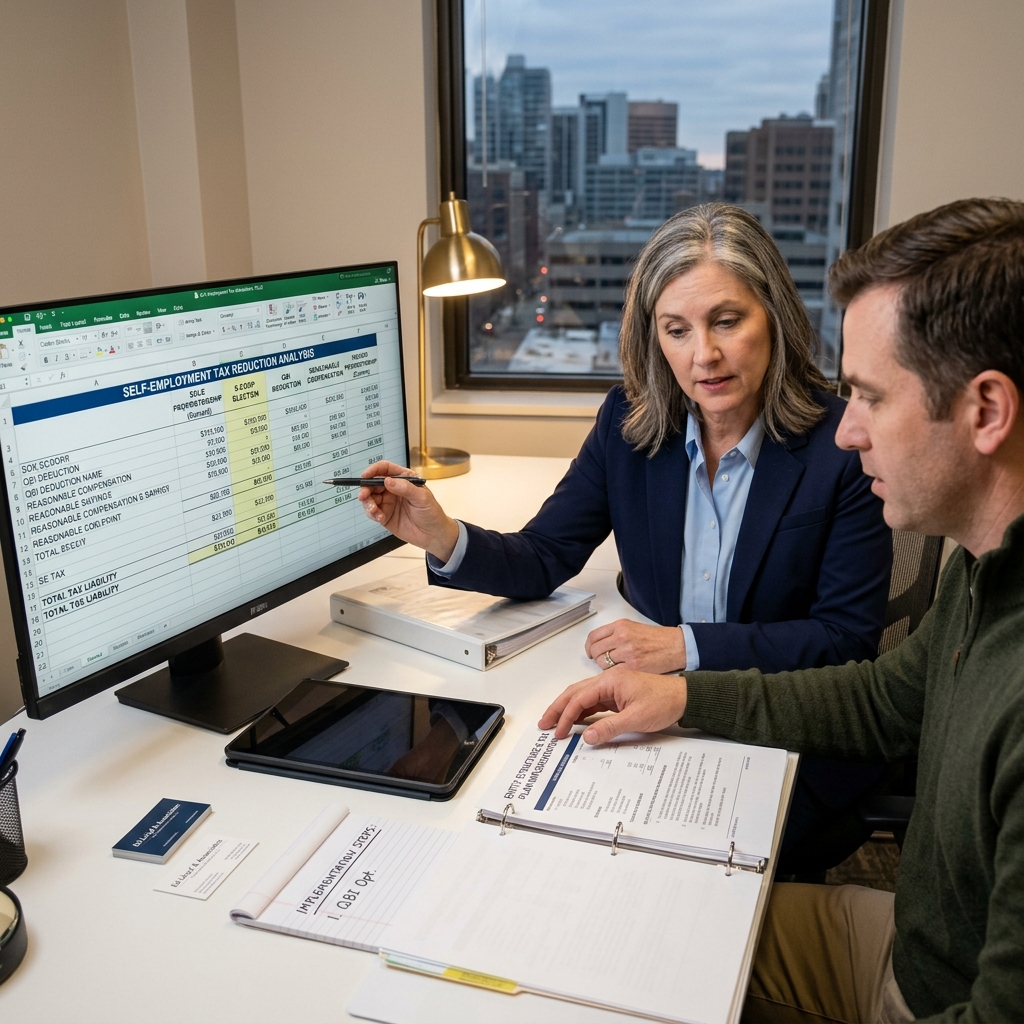

S-Corp Election (most common for service businesses) Convert your existing entity to be taxed as an S-Corporation. You become an employee of your own business and pay yourself reasonable W-2 wages. The remaining profit flows through as a distribution, which avoids self-employment tax entirely on that portion.

C-Corporation (less common, specific situations) Used when you want to retain earnings in the business, have significant deductible losses to offset, or plan to eventually sell the business. Corporate tax rates and structure create savings in particular scenarios.

Partnership or Multi-Member LLC (scaling businesses) If you have partners or plan significant growth, these structures offer flexibility in income allocation and can reduce overall self-employment tax burden when structured correctly.

The critical number here is “reasonable compensation.” IRS rules require S-Corp owners to pay themselves a reasonable W-2 wage for services rendered. You can’t just take $50K in wages and $350K in distributions. But you also don’t have to pay yourself every dollar as W-2 wages. The sweet spot varies by industry and role, but typically ranges from 40-60% of total net profit as wages, with the remainder as distributions.

Your action: evaluate which entity structure fits your current business size, profit level, and growth plans. The wrong choice costs tens of thousands annually.

S-Corp Election Strategy for Maximum Savings

This is the workhorse strategy for service business owners earning $500K+ in net income. We implement this more than any other tactic because the math is straightforward and the savings are material.

Here’s the mechanics: you elect S-Corp taxation (typically filed on Form 2553 if you’re already an LLC, or by default if you form a new S-Corp). You establish yourself as an employee. You pay yourself a reasonable W-2 salary. The remaining profit—sometimes 40-50% of total net income—distributes to you as a shareholder distribution.

The payoff: that distribution avoids the 15.3% self-employment tax entirely.

On $400K of net profit, if you pay yourself $200K in W-2 wages and take $200K as distributions:

- Self-employment tax under sole proprietor: ~$56,800

- Self-employment tax under S-Corp: ~$15,300 (on wages only)

- Annual savings: ~$41,500

Results mentioned are not typical and individual results will vary based on your specific situation. Your actual numbers depend on your profit level, the reasonable wage for your role, and your state tax situation.

The implementation matters. You need payroll processing, quarterly filings, and slightly more accounting complexity. But for owners in your income bracket, the ROI is immediate and substantial.

Your next step: if you’re not already in S-Corp status, have a conversation with your CPA about whether the election makes sense for your business.

Qualified Business Income Deduction Optimization

The QBI deduction (Section 199A) allows eligible business owners to deduct up to 20% of qualified business income. But high-income earners face limitations.

For 2026, the QBI deduction phases out for service businesses earning over roughly $230K (single) or $460K (married). Once phased out, the deduction disappears unless you meet material participation tests. This is where most high-income owners get blindsided.

Material participation means you’re actively involved in running the business, typically documented through the 100-Hour Test or other IRS methods. Service business owners almost always qualify. The issue isn’t meeting the test; it’s understanding that it exists and documenting your involvement.

We pull back the curtain here: many owners let this deduction slip away simply because they didn’t know they needed to track their participation hours or didn’t understand the phase-out thresholds.

The optimization strategy involves:

- Documenting your material participation with time records or contemporaneous logs

- Understanding how business structure (S-Corp vs. partnership) affects QBI calculation

- Potentially timing certain income or deductions to maximize the deduction in specific years

Your action: if you earn over $230K (single) and haven’t been documenting material participation, start now. Pull time records for 2026. Your CPA can evaluate whether you qualify, but you need the evidence.

Expense Categorization and Deduction Maximization

This is tactical blocking and tackling, but it separates owners who keep more of what they earn from those who leave money on the table.

Most service business owners claim basic deductions: office rent, software subscriptions, equipment, maybe some travel. But there’s a deeper layer of deductions they miss.

Consider these often-overlooked categories:

Professional development and education Courses, certifications, coaching, mastermind groups. All deductible if they maintain or improve skills related to your business.

Business use of home If you have a dedicated office space, you can deduct a portion of rent, utilities, and maintenance using either the simplified method or actual expense method.

Vehicle and mileage Client meetings, site visits, and business travel. Track meticulously. The standard mileage rate for 2026 gives substantial deductions if documented properly.

Health insurance and retirement contributions SEP-IRA, Solo 401(k), or S-Corp deductions. These directly reduce taxable income and build wealth simultaneously.

Meals and entertainment Changed in recent years. Current rules allow 100% deduction for business meals in certain circumstances. Know the rules; they’re stricter than you think.

Depreciation and Section 179 Equipment, technology, furniture. Accelerated deductions available through Section 179 expensing on assets up to certain thresholds.

The cumulative impact matters. A $5K deduction you missed is roughly $1,500 in federal tax savings. Miss ten of those and you’re looking at $15K in unnecessary taxes paid.

Your action: conduct a deduction audit with your CPA. Walk through the past two years and identify categories you’ve been under-utilizing. Implement systems now to track these going forward.

Timing Strategies for Estimated Tax Payments

Estimated tax payments are a lever most owners ignore. But if you’re paying quarterly blindly, you’re missing optimization opportunities.

Here’s the dynamic: owners typically calculate estimated taxes based on prior-year income or make safe-harbor payments. But if your income is volatile or you’re implementing new deductions or entity structures mid-year, this approach leaves gaps.

The strategy involves analyzing your year-to-date income and making strategic adjustments to remaining quarterly payments. If you’ve implemented an S-Corp election, for example, your Q3 and Q4 estimates might drop dramatically because you’re reducing self-employment tax.

Conversely, if you’ve accelerated income recognition or delayed deductions in a particular quarter, your estimate for that quarter should reflect it.

We’ve seen owners waste $20K-$40K annually by making equal estimated payments all year when their actual tax liability was front-loaded or back-loaded. Recalibrate mid-year.

Safe harbor rules exist (pay 90% of current-year tax or 100% of prior-year tax), so you won’t face penalties if you adjust strategically within those bounds.

Your action: don’t just cut a check every quarter on autopilot. In June and September, review your year-to-date income and adjust your Q3 and Q4 estimates accordingly.

Building Your Year-Round Tax Advisory Foundation

This is where we distinguish between tax preparation and tax strategy. Many owners work with a CPA once a year at filing time. That’s reactive. It’s also expensive.

Strategic tax planning requires ongoing visibility into your business performance. We implement quarterly business reviews where we monitor profit trends, track progress toward deduction targets, and adjust strategy as your situation evolves.

Here’s what a proactive tax advisory foundation includes:

Monthly or quarterly bookkeeping Clean books give you real-time visibility. You know your actual profit, not an estimate, when decisions need to be made.

Quarterly tax reviews Strategic check-ins to evaluate whether your current structure is optimal and whether new opportunities have emerged.

Year-end planning conversations Before December 31, we identify what moves make sense to finalize in the current year (accelerating or deferring income, maximizing deductions, adjusting W-2 wages if you’re in an S-Corp).

Ongoing education Tax law changes constantly. A good advisor keeps you informed about changes that affect your specific situation.

The investment in proactive advisory is typically $3K-$7K annually depending on complexity. That sounds high until you realize it routinely unlocks $50K-$100K in savings that wouldn’t happen otherwise.

Our CPA tax reduction services are designed around this philosophy. We’re not bill-by-the-hour gatekeepers. We’re partners in your tax reduction strategy.

Your action: if your current relationship is transactional (you drop off documents in January, get a return in March), it’s time to explore a different model.

Common Mistakes High-Income Service Owners Make

We’ve seen the patterns repeat across hundreds of clients. Here are the biggest wealth-draining errors:

Ignoring entity structure until it’s too late Owners wait until revenue hits $1M+ to consider S-Corp status. By then, they’ve overpaid $100K+ in unnecessary self-employment tax. Start earlier.

Paying themselves all W-2 wages in an S-Corp If you’re in an S-Corp but paying 100% of profit as W-2 wages, you’ve eliminated the tax benefit entirely. The IRS will scrutinize this. Find the right balance.

Losing deductions due to poor documentation “I think I spent $15K on education this year” isn’t good enough. Documentation matters. No receipt, no deduction.

Conflating business expenses with personal spending The line blurs easily in service businesses. A business meal, a work trip, a home office. Document the business purpose clearly.

Deferring all tax decisions to April By then, your income for the year is locked. You’ve missed twelve months of optimization opportunities. Engage quarterly instead.

Underestimating self-employment tax impact Many owners calculate federal income tax but forget to factor in self-employment tax when deciding whether a business decision makes sense. It’s 15.3% on top of everything else.

Your takeaway: these mistakes are all preventable with the right structure and attention. You don’t need to be brilliant to avoid them. You just need intentionality.

Taking Action: Your Path to Significant Tax Reduction

Cutting self-employment tax by $100K+ isn’t theoretical. We do it routinely for service business owners in your bracket. But it requires moving from awareness to action.

Here’s your immediate path forward:

Step 1: Audit your current structure Are you a sole proprietor, single-member LLC, or already in S-Corp status? If you’re not in S-Corp status and earning $400K+, you’re almost certainly overpaying.

Step 2: Calculate your potential savings Take your current net profit. Estimate what portion could reasonably become a distribution instead of self-employment income. Multiply by 15.3%. That’s your annual opportunity.

Step 3: Consult your CPA Discuss S-Corp election, reasonable wage thresholds for your industry, and the implementation timeline. Some elections are effective retroactively to January 1; others take effect when filed.

Step 4: Build the operational foundation If you elect S-Corp status, you’ll need payroll processing and adjusted accounting. It’s not complicated, but it requires systems.

Step 5: Implement quarterly reviews Schedule quarterly conversations with your tax advisor to monitor progress, catch opportunities, and adjust course as needed.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

The owners who keep the most of what they earn aren’t necessarily the ones making the highest income. They’re the ones who are intentional about structure, disciplined about documentation, and proactive about strategy. That’s where we come in. If you’re ready to unlock the playbook and stop leaving six figures on the table, let’s talk.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

Can we really help service business owners cut their self-employment tax by $100K or more?

Yes, we work with service-based business owners who have $2M+ in revenue and $500K+ in taxable income, and we regularly structure strategies that reduce their tax burden by 50% or more. The key is pulling back the curtain on how entity structure, qualified business income deduction optimization, and strategic expense categorization work together. We’re transparent that results aren’t typical and depend entirely on your specific situation, so we always recommend consulting with a qualified tax professional before implementing any strategy we recommend.

What makes your approach different from standard tax preparation?

We don’t just prepare your taxes after the fact like most firms do. We proactively structure your business throughout the year to minimize what you owe, then monitor your performance to catch optimization opportunities before they slip away. Our Tax Strategist works with us to analyze your numbers quarterly, identify deduction gaps, and adjust your strategy based on your actual earnings rather than guessing at estimated tax payments.

How do we know which tax strategy will work best for our specific business?

We start by understanding your service business model, your current entity structure, and your taxable income level, then we evaluate whether an S-Corp election, strategic expense categorization, QBI deduction optimization, or a combination of approaches makes sense for you. This information is for educational purposes only and does not constitute tax, legal, or financial advice, so we always work alongside your existing advisors to build a coordinated strategy tailored to your situation.

Recent Comments