Table of Contents

- The Hidden Opportunity: Why Service Owners Leave Thousands on the Table

- Understanding What Qualifies for Reclamation and Recovery

- Audit Your Past Three Years: Where the Money Really Went

- Identifying Red Flags That Signal You Overpaid

- The Amendment Process: How We File for Maximum Recovery

- Documenting Your Case: Building an Audit-Proof Position

- Strategic Timing: When and How to File Your Claims

- Common Mistakes That Kill Your Reclamation Chances

- Why DIY Reclamation Efforts Typically Fail

- Your Next Steps: How We Help You Keep What You Earned

- Frequently Asked Questions (FAQ)

The Hidden Opportunity: Why Service Owners Leave Thousands on the Table

You’re profitable. Your business runs well. But at tax time, you write a check that makes you wince—and you suspect something’s off.

You’re not paranoid. Most service-based business owners with $2M+ in revenue are overpaying income taxes by thousands, sometimes hundreds of thousands of dollars annually. The culprit isn’t complicated: it’s aggressive tax planning that never happened in the first place.

Here’s what we see repeatedly. Business owners focus on growing revenue, managing operations, and keeping clients happy. Tax strategy? It gets pushed to April. That’s when a tax preparer files whatever deductions and structures are obvious, misses opportunities that require planning, and calls it done. The result: you pay far more than you legally owe.

The good news is simple. Federal tax law allows business owners to reclaim overpaid taxes through amended returns going back three years. You don’t need permission from the IRS. You don’t need to wait for an audit. If you overpaid, you can pull back the curtain on what went wrong and fix it immediately.

The first step is understanding that reclamation isn’t about bending rules—it’s about using the rules correctly.

Understanding What Qualifies for Reclamation and Recovery

Not every tax payment can be recovered. Understanding what the IRS considers a legitimate reclamation claim separates real opportunity from wishful thinking.

Reclamation claims rest on three pillars: missed deductions, incorrect entity structure, and passive-loss conversions. Each is grounded in tax code, each can be supported by documentation, and each requires a specific filing approach.

Missed deductions are the most common recovery target. Service businesses often fail to capture home office deductions, vehicle expenses, depreciation on equipment, professional development, and business-use technology costs. If you provided services from home, used your personal vehicle for client work, or purchased software for business operations, these likely went unclaimed.

Entity structure problems run deeper. A sole proprietor operating as an S-Corp equivalent but never electing S-Corp status leaves substantial self-employment tax on the table. The fix isn’t complicated, but it requires amending prior years and potentially filing Form 2553 to establish retroactive election dates.

Passive-loss conversions are more technical. If you own rental properties, investment real estate, or passive business interests alongside your service business, you may qualify to turn passive losses into active losses through material participation testing. This can unlock substantial deductions you couldn’t previously claim.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy.

Audit Your Past Three Years: Where the Money Really Went

The three-year window is your leverage. Under federal statute, you can file amended returns (Form 1040-X for individual filers, Form 1120-X for entities) for the prior three years and reclaim overpaid taxes plus interest.

Start by pulling your last three years of tax returns and comparing them to your actual business records. This audit reveals gaps immediately.

Open your bookkeeping files, invoices, and expense records for years one, two, and three back. Match what you actually spent against what appeared on your returns. Most owners find 15-30% discrepancies in claimed business expenses versus documented expenses.

Create a simple three-column spreadsheet:

- Column A: Expense category (vehicles, home office, professional services, software, travel, meals, depreciation)

- Column B: Amount actually documented in records

- Column C: Amount claimed on tax return

The gaps in Column C versus Column B are your initial reclamation targets.

Pay special attention to years where your business grew significantly. Growth years often see the largest planning gaps because your accountant was working from outdated assumptions about your business structure and operations.

Identifying Red Flags That Signal You Overpaid

Certain patterns consistently appear in overpaid-tax situations. Recognizing them accelerates your reclamation process.

Red flag one: No home office deduction despite working from home. If you operate from a dedicated space and never claimed home office expenses, you left money on the table every single year. The deduction is defensible, well-documented in tax code, and commonly underutilized.

Red flag two: Vehicle and mileage expenses missing entirely. Service providers (consultants, contractors, coaches, therapists, designers) drive extensively for client work. If your return shows zero vehicle expenses but you own a car or truck, that’s a reclamation opportunity.

Red flag three: Depreciation schedules that haven’t been updated. Equipment purchases, computer systems, office furniture, and vehicles all depreciate. If your returns haven’t claimed depreciation, or if depreciation stopped years ago, you’re leaving annual deductions unused.

Red flag four: Business travel, meals, and conference attendance that weren’t deducted. Owners often assume these are too risky to claim or forget to track them. When properly documented, they’re solid deductions.

Red flag five: No Section 179 election or bonus depreciation on recent equipment purchases. These mechanisms allow immediate deductions for capital purchases instead of spreading them across multiple years. Missing these converts deferred deductions into immediate value.

Red flag six: Massive W-2 withholding or quarterly tax payments with no corresponding deductions that reduce taxable income. This signals a structural problem: your business isn’t sheltering income through available deductions or entity elections.

Each red flag represents a specific recovery path.

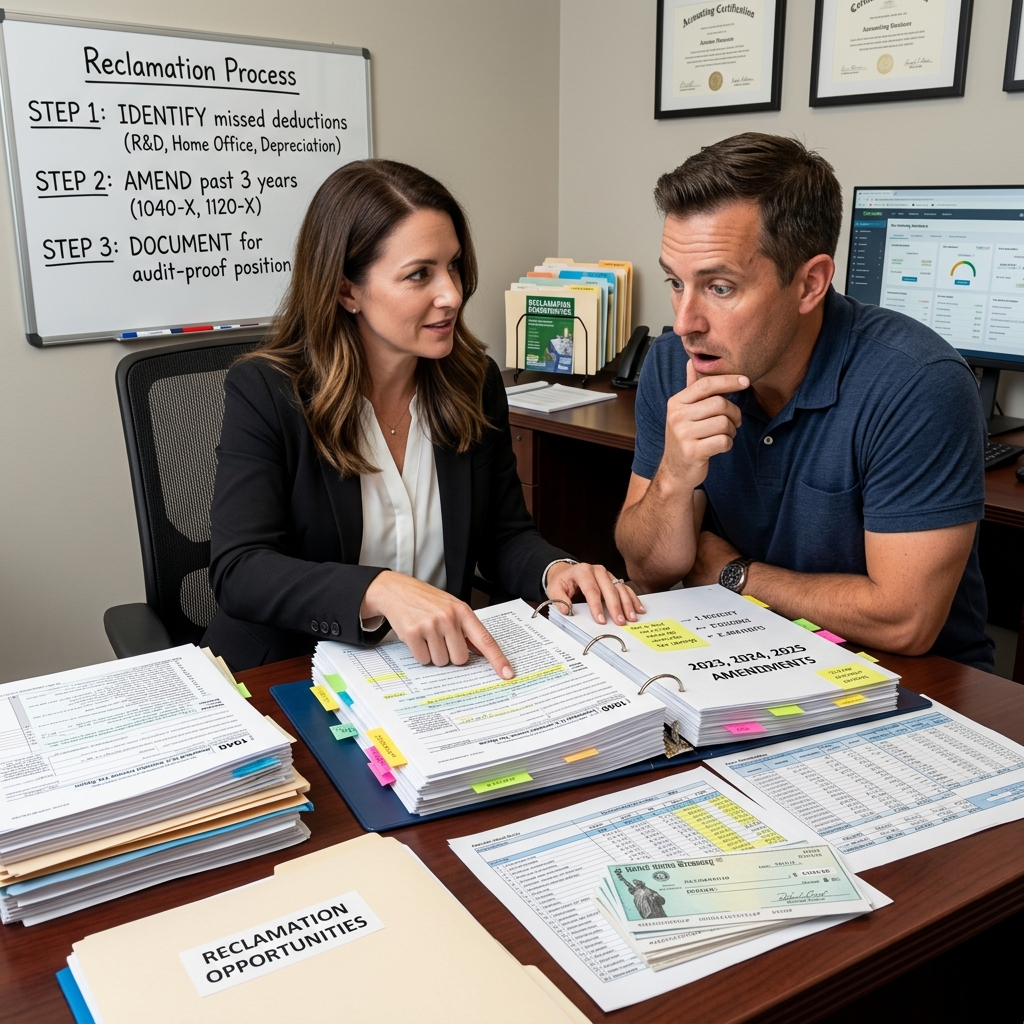

The Amendment Process: How We File for Maximum Recovery

Filing for reclamation requires precision. A sloppy amendment invites IRS scrutiny. A well-constructed amendment resolves cleanly.

The amendment process has five concrete steps.

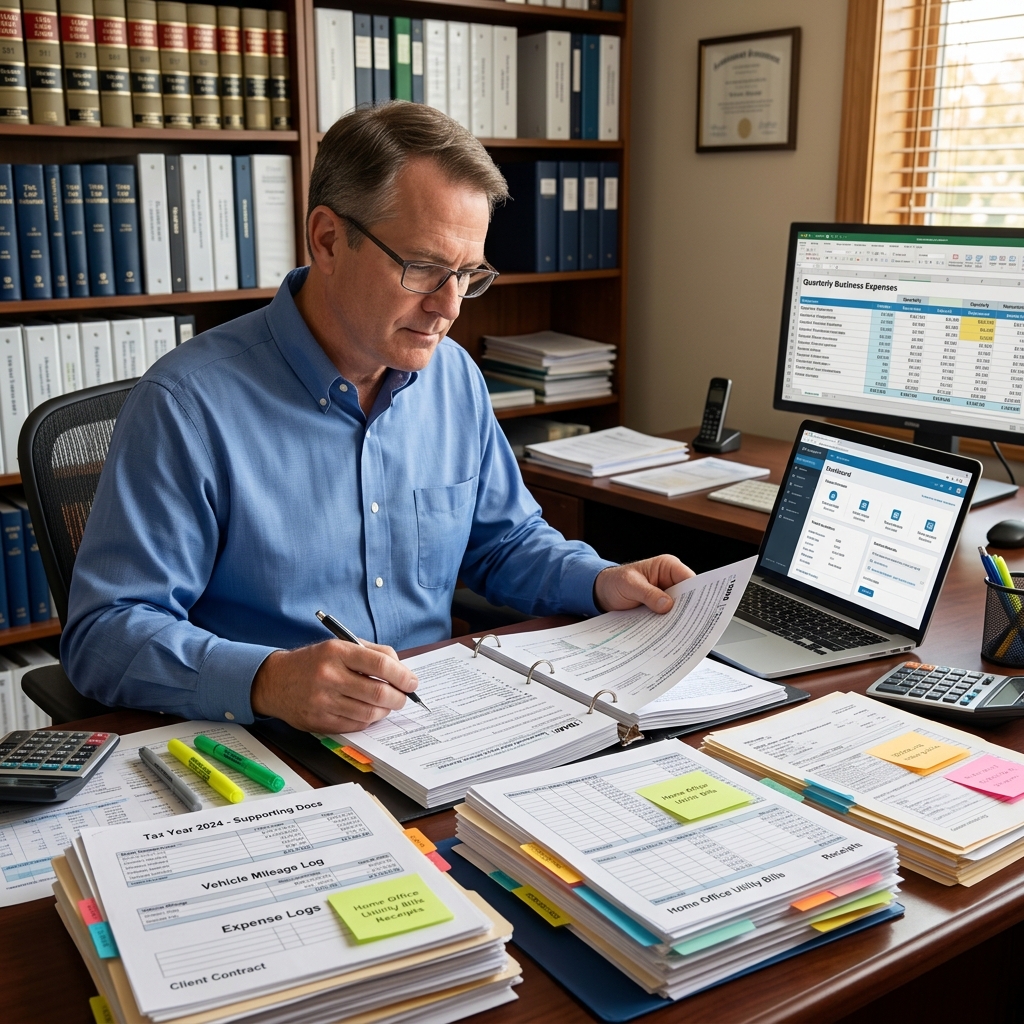

Step one: Gather complete documentation. Before filing a single form, compile supporting evidence for every adjustment you’re claiming. Invoices, receipts, mileage logs, depreciation schedules, property records—everything that substantiates your claim. The IRS doesn’t require you to attach all of it to Form 1040-X, but you must have it ready if questions arise.

Step two: Calculate the specific adjustments. Work backward from your prior return. Identify each item you’re adding or correcting. Calculate the exact dollar impact on your adjusted gross income and taxable income. Small errors compound across three years of filings.

Step three: File amended returns in the correct sequence. If you’re amending three years, file the oldest year first. This prevents timing confusion and ensures prior-year adjustments flow into subsequent years if they’re interrelated (like depreciation carryforwards).

Step four: Include detailed explanation schedules. Form 1040-X alone tells the IRS what changed—not why. Attach a separate schedule explaining each major adjustment, the tax code section supporting it, and the documentation backing it up. This transparency accelerates processing and reduces requests for additional information.

Step five: File through certified mail with return receipt. Track exactly when the IRS receives your amended return. This creates a paper trail and confirms filing dates for statute-of-limitations purposes.

Processing times vary. Simple amendments typically resolve within 8-12 weeks. Complex amendments involving entity restructuring or substantial depreciation recalculations may take 6 months.

We guide clients through every step, handling the technical calculations and IRS correspondence so you focus on your business.

Documenting Your Case: Building an Audit-Proof Position

Documentation separates defensible reclamation claims from risky ones.

Build your case around three types of records: transactional documentation, contemporaneous evidence, and regulatory support.

Transactional documentation includes the original receipts, invoices, and payment records that prove you incurred the expense. Credit card statements, bank transfers, and canceled checks all serve this purpose. For vehicle expenses, maintain a mileage log showing date, destination, business purpose, and miles driven. For home office, photograph your dedicated workspace and document its square footage.

Contemporaneous evidence is material you created at or near the time the expense occurred—not afterward. A diary entry written during travel, a project invoice dated when you performed the work, or an email confirming attendance at a professional conference all count as contemporaneous. The IRS values these because they can’t be fabricated for audit purposes.

Regulatory support means the specific tax code sections, IRS revenue rulings, and court precedents that justify your deduction. Your amended return should cite these. A home office deduction cites IRC Section 280A. Vehicle deductions cite Section 162. This foundation makes your claim look professional and informed.

The strongest reclamation cases combine all three. You have the original receipt (transactional), notes from the day proving business purpose (contemporaneous), and a citation to the applicable code section (regulatory support).

Strategic Timing: When and How to File Your Claims

Timing matters more than you might think.

The statute of limitations for amended returns is generally three years from the original filing date. If your 2023 return was filed April 15, 2024, you have until April 15, 2027 to file an amended version. After that deadline passes, the IRS won’t process your claim.

But don’t wait until the deadline. Here’s why.

Filing early accomplishes two things. First, it shortens your wait for a refund. If you file an amendment in January, you may receive your refund by March. If you file in March, you’ll wait until June or later. Second, early filing demonstrates confidence. Returns filed months before the statute expires appear more routine to the IRS than returns filed in the final weeks.

We recommend filing amendments in the first quarter of the year, immediately after finalizing your prior-year records and confirming all adjustments. This gives maximum processing time and ensures refunds arrive before the next tax season.

If you’ve already identified overpayment but haven’t filed, don’t delay. Every week increases your statute-of-limitations risk. A three-year window closes faster than you’d expect.

Common Mistakes That Kill Your Reclamation Chances

Missteps in the reclamation process invite IRS denial and missed opportunities.

Mistake one: Filing amendments without updated depreciation schedules. Many owners amend their returns to claim deductions but forget to file the depreciation schedules (Form 4562) supporting capital asset deductions. The amendment alone doesn’t communicate the full picture. Always file amended depreciation schedules alongside amended individual returns.

Mistake two: Claiming aggressive adjustments without documentation. An $8,000 home office deduction looks reasonable. An $8,000 home office deduction with no photographs, square footage calculations, or mortgage statements looks fabricated. Always lead with evidence.

Mistake three: Treating unrelated business expenses as business deductions. A meal with a friend who happens to be a business contact isn’t a deductible meal. A hotel stay for a conference you didn’t attend isn’t travel. The IRS trains auditors to spot these. If you’re unsure whether something qualifies, ask a tax professional before claiming it.

Mistake four: Filing amendments for years outside the three-year window. Some owners believe older years can be amended indefinitely. They can’t. The three-year statute is firm. After it passes, filing an amended return wastes time and gets rejected automatically.

Mistake five: Failing to address prior-year audit adjustments. If the IRS previously disallowed a deduction on your 2023 return, amending a subsequent year won’t revive it. You’d need to file a claim for refund, which is a different process entirely. Don’t conflate the two.

Mistake six: Not converting passive losses into active losses when material participation qualifies. If you own a rental property and also materially participate in managing it (meeting the 100-Hour Test or another material participation standard), you can potentially convert passive losses into active losses. Missing this conversion leaves substantial deductions on the table.

The stakes compound. One mistake in year one creates cascade errors in years two and three.

Why DIY Reclamation Efforts Typically Fail

You could attempt reclamation yourself. Many owners do. Most regret it.

The three biggest reasons DIY efforts fail boil down to complexity, risk, and opportunity cost.

Complexity. Tax code is dense. The rules for depreciation, passive losses, entity elections, and entity conversions require specialized knowledge. A missed detail doesn’t just cost you a deduction—it can expose your entire amended return to closer IRS scrutiny. One miscalculation of depreciation basis or passive loss documentation can trigger an audit of all three amended years.

Risk. Filing amended returns without professional guidance exposes you to penalties if adjustments are later disallowed. The IRS can assess accuracy-related penalties up to 20% of underpaid tax for “substantial understatement” of income tax. A DIY amendment lacking proper support can trigger these penalties, costing you more than the deduction was worth.

Opportunity cost. The time required to gather documentation, understand tax code, complete forms correctly, and track IRS correspondence is substantial. A business owner billing $200/hour loses $2,000 in billable time for every ten hours spent on reclamation. That math doesn’t work, even if you get 80% of it right.

We handle the complexity and risk. We know exactly which deductions the IRS scrutinizes most closely and which require bulletproof documentation. We file amendments confidently because we’ve done this thousands of times.

Your Next Steps: How We Help You Keep What You Earned

Reclamation isn’t theoretical. It’s a concrete process with a specific dollar outcome. We’ve helped service-based business owners recover six figures in overpaid taxes through this exact playbook.

Results mentioned are not typical and individual results will vary based on your specific situation.

Here’s exactly what happens when you work with us.

Week one: We conduct a tax history audit. You provide three years of tax returns and bookkeeping records. We analyze them against the red flags outlined above and identify reclamation targets.

Week two: We prepare a reclamation summary. This document lists every deduction, adjustment, and entity structure issue we’ve identified, along with estimated tax recovery for each year. You review it, ask questions, and approve the strategy.

Week three: We gather documentation. You provide supporting materials—receipts, invoices, mileage records, property photos, and anything else substantiating our adjustments. We organize it and cross-reference it to our amended returns.

Week four and beyond: We file amended returns with complete schedules, detailed explanations, and professional presentation. We track the IRS response and handle any inquiries.

The entire process typically takes 4-8 weeks from start to amended return filing.

Most clients see refunds within 8-16 weeks of filing. Those refunds represent actual overpaid taxes you earned the right to claim three years ago. They’re not windfalls—they’re corrections.

To start the process, reach out to our team. Bring your last three years of tax returns and any sense that you’re overpaying. We’ll pull back the curtain on exactly how much you’re leaving on the table and show you a clear path to keep more of what you earn.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

How much can we typically recover for service business owners?

We’ve helped service-based business owners reduce income taxes by 50% or more, but this information is for educational purposes only and does not constitute tax, legal, or financial advice. Results mentioned are not typical and individual results will vary based on your specific situation. Our experience shows that owners with $2M+ in revenue and $500K+ in taxable income often have significant recovery opportunities because they typically haven’t optimized their tax position. Always consult with a qualified tax professional before implementing any tax strategy.

Can we amend returns from previous years to reclaim overpaid taxes?

Yes. We specialize in identifying overpayments in your past three years of returns and filing amendments to recover what you’ve lost. The amendment process requires precise documentation and strategic timing to withstand IRS scrutiny, which is why our approach focuses on building an audit-proof position from the ground up. We handle the technical filing work while you focus on running your business.

Why do most service owners fail at reclaiming taxes on their own?

DIY reclamation efforts typically fail because business owners lack visibility into which deductions and strategies apply to their specific situation, miss critical red flags that signal overpayment, and don’t understand the documentation required to defend their position under IRS review. We pull back the curtain on where your tax dollars actually went and unlock the playbook most service owners never see. That’s how we help you keep more of what you earn.

Recent Comments