Table of Contents

- The Compensation Trap Most Service Business Owners Fall Into

- Why Your Current Pay Structure Is Costing You Hundreds of Thousands

- How the IRS Defines Reasonable Compensation and Why It Matters

- The Power of Strategic Salary Splitting for Maximum Tax Efficiency

- Dividend Distributions vs. W-2 Wages: Building Your Optimal Compensation Mix

- Entity Structure Decisions That Make or Break Your Tax Position

- Real Numbers: What Profitable Service Businesses Actually Keep After Strategy

- Quarterly Tax Planning: Staying Ahead of Estimated Payments

- Common Compensation Mistakes That Trigger Audit Risk

- Building Your Year-Round Advisory Relationship for Ongoing Optimization

- Frequently Asked Questions (FAQ)

The Compensation Trap Most Service Business Owners Fall Into

You’re probably taking a straight W-2 salary from your business. It feels safe. It’s what you’ve always done. And it’s costing you a fortune.

Most service business owners we work with operate under a fundamental misunderstanding: they believe their business structure and compensation method are locked in stone. They pay themselves one way because that’s how they set it up years ago, and they assume the IRS would object to anything more creative.

The reality is different. The IRS doesn’t care how you pay yourself, as long as you follow specific rules. What they do care about is that you’re aware of those rules and intentionally choosing a strategy rather than defaulting to the easiest option.

Here’s what we see repeatedly: A service business with $3M in revenue and $800K in taxable income pays the owner a $400K W-2 salary and leaves $400K sitting in the business as profit. That profit gets taxed at the corporate level, then taxed again when distributed. Total tax impact: devastating.

The trap isn’t complexity. It’s invisibility. You don’t know what you don’t know, so you never question the structure you inherited or built by accident.

Your move: Schedule a conversation with a tax strategist who understands service businesses. The structure you have now is almost certainly not your best option.

Why Your Current Pay Structure Is Costing You Hundreds of Thousands

Let’s pull back the curtain on the math.

Assume you’re an S-corp or C-corp owner with $2.5M in revenue and $600K in taxable income. You take a $350K W-2 salary. You leave $250K in the business as retained earnings or distributions.

That $250K sitting in your business gets hit multiple times:

- Federal income tax on corporate profit (21% federal rate for C-corps)

- State income tax (varies, but often 5-8%)

- Self-employment or net investment income tax (3.8% NIIT)

- Then when you eventually distribute it, potentially another round of taxation

A $250K profit can easily cost $100K+ in cumulative taxes depending on your state and structure.

Now flip the scenario. What if you’d split your compensation differently at the year’s beginning? Instead of taking $350K W-2 and leaving $250K in retained earnings, you strategically allocate compensation to minimize the total tax burden across federal, state, self-employment, and pass-through taxes.

The difference isn’t small. Across multiple service business owners we’ve advised, the shift from a single-wage approach to a strategically split compensation model yields 15-30% tax reductions in year one. Some clients keep an additional $100K-$300K annually.

Results mentioned are not typical and individual results will vary based on your specific situation.

What to do next: Calculate your current effective tax rate on business income. If it’s above 40%, your structure is likely inefficient.

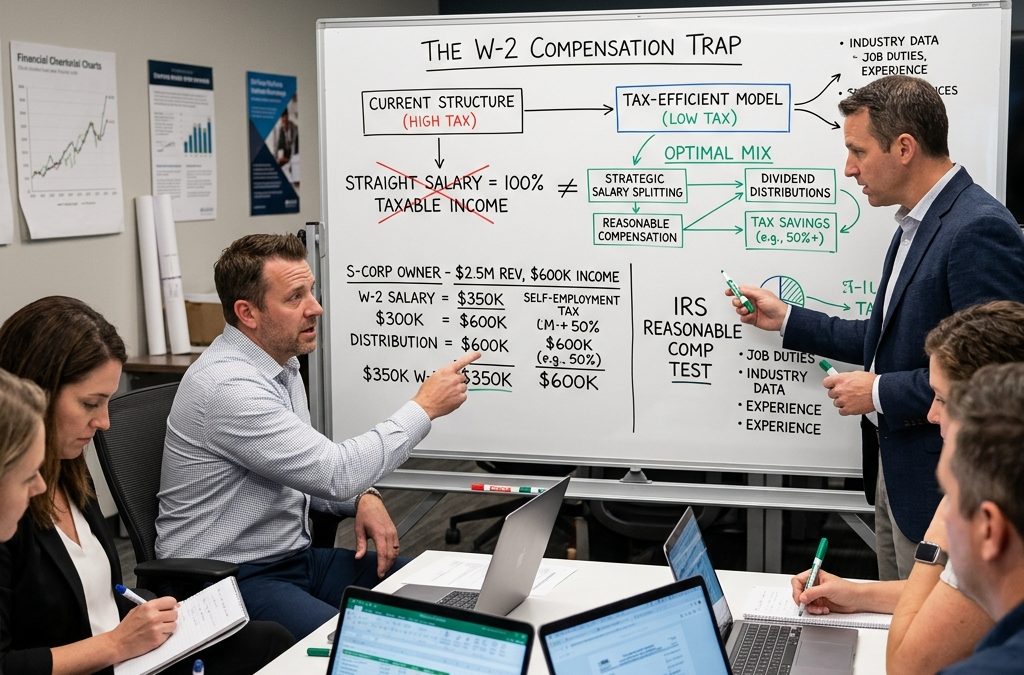

How the IRS Defines Reasonable Compensation and Why It Matters

The IRS has one hard requirement for owner compensation: it must be “reasonable.”

That word terrifies most business owners. It sounds vague. It sounds like the IRS can challenge you arbitrarily. But reasonable compensation has a specific meaning in tax law, and understanding it unlocks everything.

Reasonable compensation means you pay yourself what someone in your role, with your experience and responsibilities, would earn in a similar business. A surgeon-owner pays themselves like a surgeon. A consultant-owner pays themselves like a consultant. A marketing agency owner pays themselves like a marketing executive.

Here’s what it’s not: It’s not the minimum amount you can get away with. It’s not a trick. It’s literally the market rate for your work.

The IRS scrutinizes this specifically for S-corp owners who try to minimize W-2 wages and maximize distributions. If you own a management consulting firm pulling $1M in annual profit and only pay yourself a $50K W-2, you’ll get audited. That’s not reasonable; that’s obvious tax avoidance.

But if you pay yourself $180K W-2 (market rate for a principal consultant) and take the remaining $820K as a distribution? That’s defensible because your W-2 matches your actual role and value.

The 100-Hour Test is one useful benchmark: If you work more than 100 hours for the business annually, you’re likely meeting material participation requirements that affect how losses and income are classified.

Actionable insight: Document comparable salaries for your role in your industry. This becomes your audit defense.

The Power of Strategic Salary Splitting for Maximum Tax Efficiency

Salary splitting means allocating your total compensation across different vehicles: W-2 wages, distributions, dividends, retirement contributions, health insurance, and other deductible benefits.

The power comes from tax rate arbitrage. W-2 wages trigger self-employment taxes (15.3% combined rate). Distributions from an S-corp don’t. But distributions must follow reasonable compensation rules. So the strategy is to maximize distributions while staying compliant with reasonable compensation standards.

Here’s a concrete example. You’re an S-corp owner with $500K in net profit. You could take $500K W-2. You’d owe:

- Income tax (25% federal + state, roughly)

- 15.3% self-employment tax

- Total: ~40% effective rate, leaving you $300K

Or you could structure it as:

- $180K W-2 (reasonable for your role)

- $320K distribution (subject to income tax but no SE tax)

- Federal + state tax on the $320K: ~25%, or $80K

- Total taxes: $45K + $80K = $125K

- Leaving you: $375K

The difference: $75K in your pocket. Every year.

That’s not tax evasion. That’s tax strategy built on reasonable compensation. This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy.

The split works because different income sources are taxed differently. Your job is to align compensation type with its tax treatment.

Next step: Model your current income split against a reasonable compensation benchmark. You might find $50K-$150K in annual savings immediately.

Dividend Distributions vs. W-2 Wages: Building Your Optimal Compensation Mix

W-2 wages and dividends/distributions serve different purposes. Understanding when to use each is the core of tax-efficient compensation design.

W-2 wages are predictable, deductible, and required at reasonable levels. They generate a payroll trail that the IRS expects to see. They also create self-employment tax liability.

Distributions and qualified dividends (if you own C-corp stock or have qualified dividends from investments) are subject to income tax only, not employment tax. But they can only come from business profit, and distributions must follow reasonable compensation thresholds.

Here’s the decision framework:

- Lock in reasonable compensation first. This is your W-2 baseline. Don’t skimp; be honest about market rates.

- Direct remaining profit to distributions. If your business generates $400K in profit beyond reasonable compensation, that $400K flows to distributions, taxed as income only.

- Layer in tax-deductible benefits. Health insurance premiums, retirement plan contributions, and other fringe benefits reduce taxable income before distributions are even calculated.

- Monitor state-level taxes. Some states tax distributions differently than wages. Virginia and California have higher thresholds. Know your state’s rules.

The optimal mix varies by business size, profitability, and state. A $2M service business in North Carolina has a different ideal structure than a $2M service business in California.

Action item: Calculate your current W-2 as a percentage of total owner compensation. If it’s more than 75% of your total comp, you’re likely leaving tax savings on the table.

Entity Structure Decisions That Make or Break Your Tax Position

Your entity structure (S-corp, C-corp, sole proprietorship, LLC taxed as S-corp, etc.) fundamentally shapes your compensation options and tax liability.

We typically see service business owners in one of three structures: S-corp (pass-through, taxed at individual rates), C-corp (double taxation, but some situations favor this), or LLC taxed as an S-corp (flexible, taxed like an S-corp).

For most service businesses with $2M+ revenue and $500K+ taxable income, S-corp treatment is optimal. Why? Because it allows reasonable W-2 compensation at market rates while distributing remaining profit without self-employment tax.

C-corp status can make sense if you’re retaining substantial profit in the business for reinvestment. The 21% corporate tax rate might be lower than your personal marginal rate. But once you distribute that profit, you hit double taxation.

The wrong structure costs money every quarter. We’ve worked with service business owners who stayed in C-corp status for years after profitability changed, paying roughly 50% more in total tax than they would have under S-corp election.

Structure decisions interact with everything else: state taxes, retirement plan options, reasonable compensation thresholds, and even audit risk. This isn’t a one-time decision. It’s a living strategy that should be reviewed annually.

Your next move: Request a structure audit from a CPA who specializes in service business owners. Determine whether your current entity class is optimal for your 2026 situation and beyond.

Real Numbers: What Profitable Service Businesses Actually Keep After Strategy

Let’s walk through a real-world scenario that reflects many of the service business owners we advise.

Business profile:

- Marketing consulting firm

- $2.8M revenue

- $850K taxable income

- Owner has 3 employees

- Operating in North Carolina

- Currently S-corp with single W-2 strategy

Current structure (year one):

- W-2 salary: $500K

- Distribution: $350K (after tax)

- Payroll taxes on W-2: ~$38K

- Federal + state income tax on $850K: ~$212K

- Total owner tax burden: ~$250K

- Owner keeps: $600K after tax

Optimized structure (year two with proper planning):

- W-2 salary: $220K (market rate for principal consultant)

- Distribution: $630K (subject to income tax only)

- Payroll taxes on W-2: ~$17K

- Federal + state income tax on total comp: ~$188K

- Total owner tax burden: ~$205K

- Owner keeps: $645K after tax

Difference: $45K additional after-tax income in year two.

Over a five-year period, that’s $225K in recovered tax dollars. Results mentioned are not typical and individual results will vary based on your specific situation.

These numbers assume proper structure, reasonable compensation documentation, and consistent year-round planning. They also assume compliance with all tax rules. The gains come from alignment, not corner-cutting.

Quarterly Tax Planning: Staying Ahead of Estimated Payments

Most service business owners think of taxes once a year, in March or April. That’s reactive. We work proactively.

Quarterly tax planning means modeling your expected profit mid-year and adjusting your compensation, retirement contributions, and distributions to optimize the full-year outcome. It sounds tedious. It saves money.

Here’s why it matters: If you wait until December to look at your numbers, you’ve already locked in much of your tax liability. Payroll has been processed. Income has been recognized. You’ve missed opportunities to defer income or accelerate deductions.

Proactive quarterly planning lets you:

- Make mid-year retirement plan adjustments (solo 401k contributions, SEP-IRA timing)

- Accelerate legitimate business expenses into the current year

- Time distributions strategically based on estimated profitability

- Adjust W-2 withholding if your business is performing better or worse than expected

- Implement losses into current-year taxes if opportunities arise

Most service businesses work with accounting firms that prepare tax returns. Few work with a tax strategist who works with them continuously. That’s the gap we fill.

What to do: Schedule quarterly check-ins with your CPA or tax advisor. Review profitability year-to-date and model compensation decisions for the remaining quarters.

Common Compensation Mistakes That Trigger Audit Risk

Aggressive positioning feels bold until the IRS knocks. Here are the mistakes we see that increase audit risk.

Mistake 1: Unreasonably low W-2 wages Taking a $50K W-2 while your S-corp generates $500K profit screams risk. The IRS knows owner compensation should track business profitability. Document market rates and stay defensible.

Mistake 2: Inconsistent compensation year-to-year If your W-2 jumps from $150K to $50K with no business reason, the IRS notices. Consistency is your friend. If compensation changes, document why.

Mistake 3: No documentation of business valuation or role justification If you’re challenged on reasonable compensation, you need comparative data: industry salary surveys, peer benchmarks, documented hours, and role descriptions. “I thought $100K was fair” won’t hold up.

Mistake 4: Mixing personal and business expenses This isn’t compensation strategy, but it kills audit defense. Keep a clean P&L. Separate personal draws from business deductions.

Mistake 5: Aggressive loss positions without material participation documentation If you’re claiming losses but spending less than 100 hours on the business, the 100-Hour Test fails. You can’t turn passive losses into active losses without evidence of involvement.

Takeaway: Audit risk drops dramatically when you’re transparent and documented. Build your strategy on evidence, not hope.

Building Your Year-Round Advisory Relationship for Ongoing Optimization

Compensation strategy isn’t a one-time event. Markets change. Business structure changes. Tax law changes. Your strategy should evolve annually.

We work with service business owners as ongoing advisors, not once-a-year tax preparers. That relationship means:

- Quarterly check-ins to adjust strategy based on profitability

- Real-time guidance when your business structure or profit changes

- Proactive planning for major business events (adding partners, selling equity, bringing in investors)

- Coordination with your accountant to ensure bookkeeping aligns with tax strategy

- Annual strategy review and optimization

The difference between advisory and transaction-based relationships is the difference between keeping an extra $50K-$150K annually and hoping your structure is right.

We specialize in service-based business owners with $2M+ revenue and $500K+ taxable income. We know your industry, your challenges, and the specific compensation levers that move your bottom line. CPA tax reduction services tailored to your business structure is where we focus.

Here’s your next move: Reach out to discuss your current compensation structure and what optimization might look like for your specific business. We’ll model scenarios and show you the dollar impact before you commit to any changes.

The service business owners we work with keep more of what they earn. Your structure can too.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

How much can we typically reduce your taxes through owner compensation strategies?

We’ve helped service business owners with $2M+ in revenue and $500K+ in taxable income reduce their income taxes by 50% or more through strategic compensation planning. Results mentioned are not typical and individual results will vary based on your specific situation. The actual savings depend on your current entity structure, compensation mix, and business profitability, which is why we conduct a thorough analysis before outlining your specific opportunity.

What’s the difference between W-2 wages and dividend distributions in our compensation strategy?

We structure your compensation around two primary levers: W-2 wages (which reduce your business income but come with payroll taxes) and dividend distributions (which avoid payroll taxes but face income tax). The optimal mix depends on your entity type, whether you’re an S-corp, and IRS rules around reasonable compensation. Our job is to pull back the curtain on how the IRS defines “reasonable” and build your compensation plan to maximize what you keep while staying compliant.

Why do we recommend quarterly tax planning instead of waiting until year-end?

We implement quarterly reviews because estimated tax payments and compensation decisions made mid-year have a compounding effect on your final tax bill. Waiting until December leaves us reactive instead of proactive, and you’ll likely overpay throughout the year. By monitoring your numbers quarterly, we adjust your compensation strategy, catch opportunities early, and ensure you’re not sending the IRS an interest-free loan.

Recent Comments