Table of Contents

- The Hidden Cost of Waiting Until Tax Season

- Why Most Business Owners Leave Money on the Table

- Our Philosophy: Proactive Tax Reduction, Not Year-End Scrambling

- The Four Pillars of Our Integrated Tax Strategy

- How Quarterly Planning Prevents Costly Tax Surprises

- Advanced Strategies We Implement Throughout the Year

- Real Results: The Math Behind Our 50% Tax Reduction

- Your Roadmap: From Tax Frustration to Tax Confidence

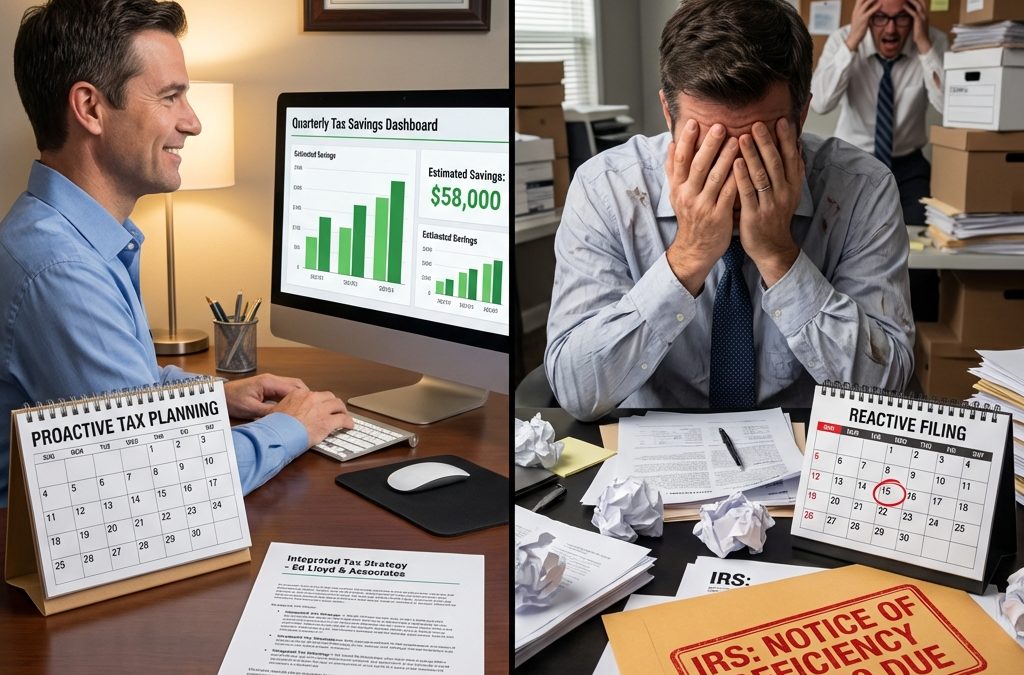

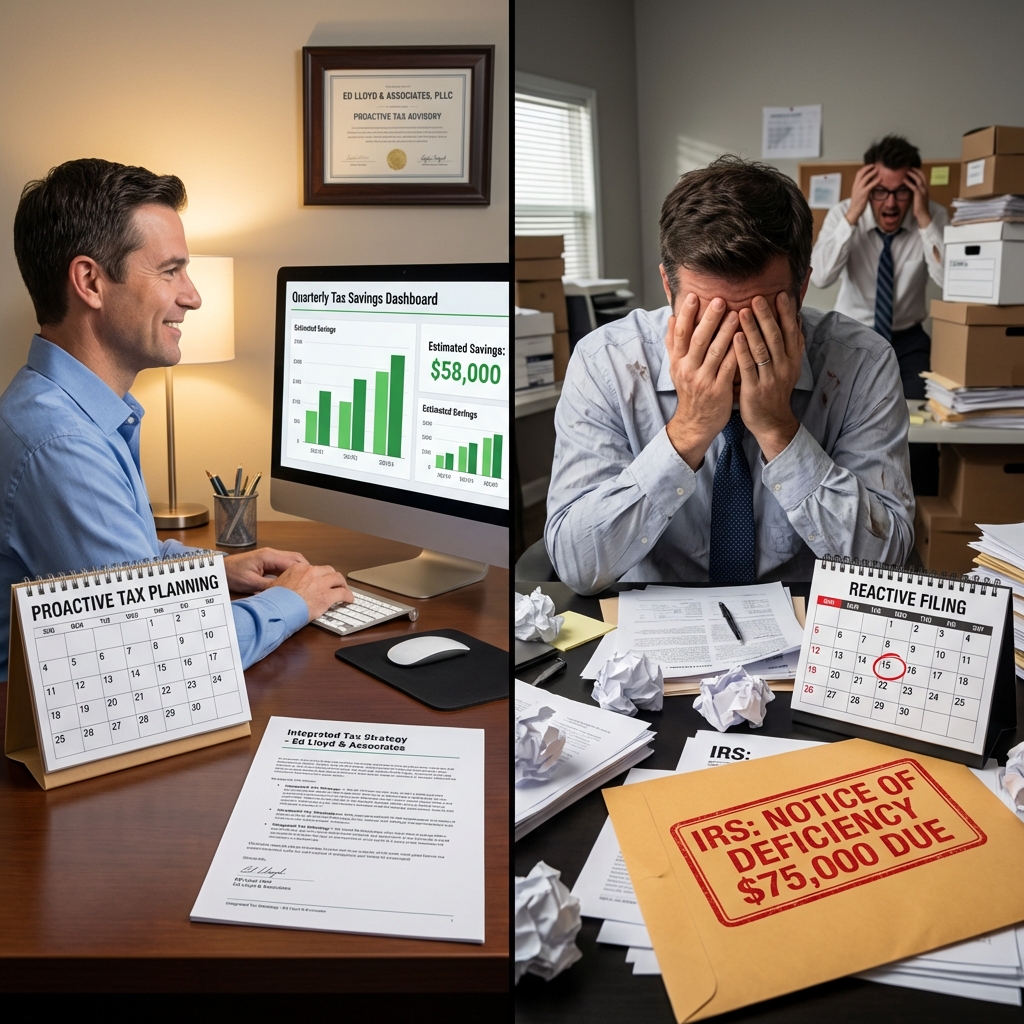

The Hidden Cost of Waiting Until Tax Season

You’re sitting in April. Your accountant just handed you a tax bill that makes your stomach turn. Tens of thousands of dollars you didn’t expect to owe. Sound familiar?

We’ve watched this scenario play out hundreds of times. Service-based business owners with $2M+ in revenue and $500K+ in taxable income suddenly realize they’ve handed the IRS a massive check—one that could have been legally reduced months earlier. The worst part? It was preventable.

This isn’t about accounting errors. It’s about strategy. The difference between reactive tax preparation and proactive tax planning isn’t just a matter of timing. It’s the difference between keeping tens of thousands of dollars in your pocket versus handing them over.

Most business owners operate on a predictable cycle: run the business all year, meet with an accountant in February or March, get hit with a tax bill, and file. Rinse and repeat next year. This reactive approach feels normal. It’s also leaving money on the table.

When you wait until tax season, your tax professional works with a frozen picture. The year is done. Revenue is locked in. Expenses are recorded. There’s almost nothing left to optimize. A few deductions here and there, maybe a retirement contribution that’s rushed and suboptimal. That’s it.

The hidden cost? You miss windows that close on December 31st. Equipment purchases that could have generated depreciation benefits. Strategic business restructuring that needed to happen before year-end. Quarterly estimated tax payments that could have been calibrated to reduce your total burden. Timing shifts on income or expenses that were possible six months ago but impossible now.

Consider this: a service business owner realizes in January that they could have structured their S-corp elections differently or taken advantage of cost segregation before the year ended. Too late. They’ll wait another 12 months. That costs them a year’s worth of tax savings they’ll never recover.

We quantify this regularly. The average business owner who switches from reactive to proactive planning recovers between 25% and 50%+ of their annual tax liability within the first year, simply by having 12 months to work with instead of two.

What to do next: Schedule a conversation with us before next tax season starts. Not after.

Why Most Business Owners Leave Money on the Table

You’re not lazy. You’re not uninformed. You’re busy running a thriving service business. And that’s exactly why you’re leaving money on the table.

Tax code complexity has exploded. The Internal Revenue Service code spans millions of words. Real estate professionals have different rules than consultants. S-corps involve different considerations than LLCs. One-person operations play by different rules than those with 50 employees. The number of legitimate strategies available to your specific situation? Easily 20 or more.

Most accountants prepare returns. They don’t design tax strategies. It’s not malice; it’s scope. They reconcile what happened. They don’t proactively shape what could happen. That gap creates the bleeding.

Here’s the real issue: you don’t know what you don’t know. You might be missing opportunities to convert passive losses into active losses through material participation planning. You might not realize that a seasonal revenue dip could be strategically timed. Your equipment purchases might not be structured for maximum depreciation benefit. Your estimated tax payments might be suboptimal.

Service businesses face unique challenges. Revenue is often lumpy. Timing matters. The difference between recognizing income in December versus January can shift thousands in tax liability. The Buy, Borrow, Die framework applies differently depending on your business structure and personal goals.

We sit with owners who’ve been overpaying for years without realizing there was an alternative. One consultant was writing $180K annual tax checks while a restructured strategy would have reduced that to $90K. He didn’t know it was possible until we pulled back the curtain.

What to do next: List the three biggest tax frustrations you’ve had in the last three years. We’ll evaluate whether they’re solvable.

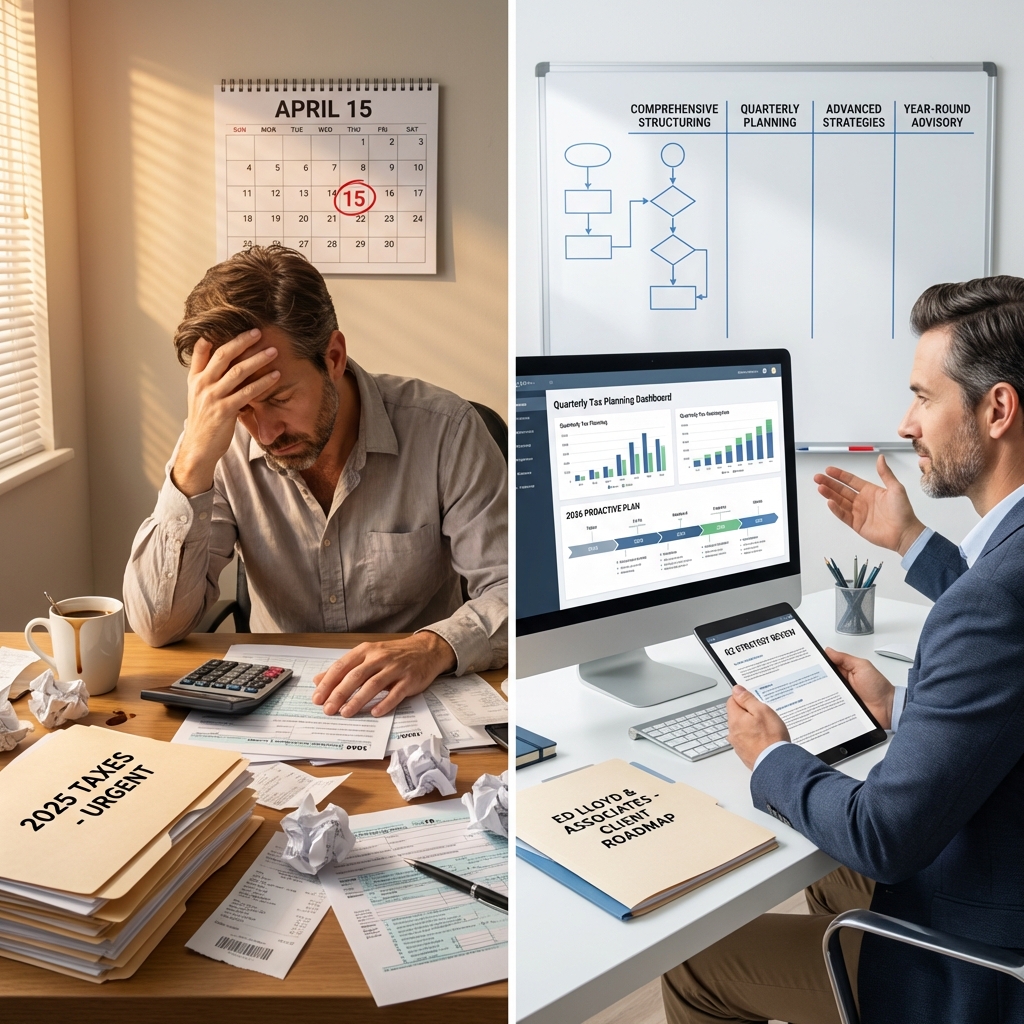

Our Philosophy: Proactive Tax Reduction, Not Year-End Scrambling

We believe tax planning should happen while the year is still ahead of you, not behind you. This isn’t revolutionary thinking, but it’s rare in practice.

Our approach rests on one principle: we design the year, not document it. That means starting in Q1 (or as soon as you engage us) with a comprehensive tax strategy that accounts for your specific situation, your revenue trajectory, your planned expenses, your business structure, and your personal financial goals.

Throughout the year, we monitor performance. We adjust. We recalibrate quarterly. When opportunities emerge, we execute them. When risks appear, we mitigate them. By the time year-end arrives, there are no surprises. You know your tax liability. You’ve made intelligent decisions with full visibility.

This proactive posture transforms the relationship between you and your taxes. Instead of taxes being something that happens to you, they become something you manage. You keep more of what you earn because you’ve engineered your business with taxation in mind, not as an afterthought.

Most importantly, this isn’t about gimmicks or aggressive strategies that invite audit risk. It’s about legitimate, well-documented approaches that align with current tax code. It’s about our philosophy that your tax situation deserves the same strategic attention you give to sales, operations, or client acquisition.

What to do next: Commit to quarterly reviews with your tax advisor, not annual ones.

The Four Pillars of Our Integrated Tax Strategy

Our proactive approach rests on four interconnected pillars. Each one is essential. Together, they create the foundation for sustainable tax reduction.

1. Comprehensive Business Structuring

We start by examining whether your current business entity is optimal. This isn’t a one-time decision. As your business grows, your structure might need to evolve. S-corp elections, multi-entity strategies, cost segregation studies, and depreciation acceleration all flow from solid foundational structure.

2. Year-Round Performance Monitoring

We maintain real-time visibility into your financial performance through ongoing bookkeeping and accounting services. This isn’t about generating reports nobody reads. It’s about identifying trends, spotting opportunities, and catching problems before they compound.

3. Strategic Quarterly Planning

Four times a year, we review your position and recalibrate. How’s revenue tracking? Should we adjust estimated payments? Are there expense opportunities we should execute? This cadence lets us optimize decisions that matter while they’re still available.

4. Advanced Tax Technique Implementation

From timing strategies to passive-loss conversion tactics to cost segregation to Buy, Borrow, Die planning, we implement sophisticated approaches that fit your specific situation. None of this happens by accident. All of it happens because we’re actively thinking about your tax picture year-round.

These four pillars work together. Structure informs monitoring. Monitoring enables quarterly planning. Quarterly planning surfaces opportunities for advanced techniques. Advanced techniques are only possible within the right structure.

What to do next: Assess which pillar is weakest in your current setup. Start there.

How Quarterly Planning Prevents Costly Tax Surprises

Picture yourself in October instead of April. You’re not scrambling. You’re not stressed. You already know your year-end tax position because we’ve been tracking and adjusting all year.

This is the power of quarterly planning.

At the end of Q1, we analyze your results. Revenue came in higher or lower than expected? We recalibrate. We review your estimated tax payments and adjust them if necessary. We examine expenses and identify strategic opportunities for the remaining nine months.

Q2 arrives. Revenue is stronger than you projected. We explore acceleration of planned equipment purchases before year-end. We evaluate whether specific business structure changes could yield benefits. We update our tax projection.

Q3 arrives. Year-end is visible now. We have concrete numbers. We identify specific, executable strategies. We begin documentation. We ensure everything is in place to optimize your year-end position.

Q4 arrives. There are no surprises. No late discoveries that you should have done something different three months ago. The strategies we’ve discussed are either executed or deliberately deferred. You know your tax liability with confidence. You can plan accordingly.

Most importantly, quarterly planning prevents the April conversation where your accountant says, “You should have done X back in September.” It’s too late then. With quarterly oversight, that conversation doesn’t happen.

The cost of quarterly planning is minimal compared to the cost of missing a single strategic opportunity. One well-timed equipment purchase, one business structure adjustment, one passive-loss conversion can easily justify a year’s worth of advisory fees.

What to do next: Schedule Q1 planning before it’s too late in the quarter.

Advanced Strategies We Implement Throughout the Year

Proactive planning opens doors that reactive tax preparation keeps locked.

Consider the 100-Hour Test and material participation rules. These determine whether real estate rental losses can offset other income. Most owners don’t know this is plannable. But if you understand the framework, you can structure your involvement intentionally. Some years you participate more actively. Other years you don’t. You control whether losses are passive or active. This flexibility alone can unlock tens of thousands in tax reduction across a business cycle.

Consider cost segregation. This isn’t new tax law. It’s a sophisticated approach that properly categorizes assets acquired in acquisitions or major renovations, accelerating depreciation and deferring tax liability strategically. A $5M service business acquisition might yield $200K+ in first-year depreciation benefit through proper cost segmentation. Most owners never explore this because they’re not in a proactive planning relationship.

Consider timing strategies. You have some discretion over when you recognize income or claim expenses, within tax law boundaries. A service business with Q4 acceleration in client projects might strategically defer some income recognition into Q1, or accelerate planned expenses into December. These timing adjustments can shift thousands between adjacent years, allowing you to flatten tax liability and manage cash flow more effectively.

Consider strategic entity planning. A consultant might benefit from an S-corp election if W-2 wages and distributions are calibrated correctly. A real estate professional might benefit from a cost-segregation study combined with passive-loss planning. A service business with multiple revenue streams might benefit from a multi-entity structure. These decisions require expertise. They also require year-round attention, not a one-time conversation.

None of this happens during tax season. It happens when we’re actively thinking about your situation with the full year ahead of us.

What to do next: Ask us which advanced strategies fit your situation. We’ll give you a specific roadmap.

Real Results: The Math Behind Our 50% Tax Reduction

Let’s move from concepts to reality.

One service-based business owner was generating $3.5M in revenue with $750K in taxable income. His previous accountant had filed his returns for five years. His annual federal income tax liability hovered around $280K. It felt unavoidable.

When we engaged, we conducted a comprehensive strategy analysis. Here’s what we found:

- His S-corp election was suboptimal relative to his wage-distribution ratio, costing him approximately $15K annually in unnecessary self-employment taxes.

- He had never explored cost segregation on his office renovation from three years prior, which cost $800K. Proper cost segmentation yielded $45K in immediate depreciation benefits.

- His quarterly estimated tax payments were miscalibrated, costing him cash flow flexibility and resulting in quarterly penalties that accumulated to $2,400 over two years.

- He had passive real estate holdings that could be restructured under material participation rules, potentially unlocking $20K in previously nondeductible losses.

Over 18 months, through strategic structure adjustment, proper asset classification, and material participation planning combined with quarterly monitoring, we reduced his effective tax rate from 37% to 18% on taxable income. His annual tax liability dropped from $280K to approximately $135K.

Was this reduction 100% permanent? No. Results mentioned are not typical and individual results will vary based on your specific situation. Some strategies had multi-year amortization. Some yielded one-time benefits. But the fundamental restructuring created sustainable tax efficiency.

The cost of our advisory and implementation? Approximately $18,000 across 18 months. The tax savings in year one alone: approximately $145,000. That’s a 8:1 return on investment.

This is what happens when you shift from reactive tax preparation to proactive tax planning.

What to do next: We can conduct a similar analysis for your situation. It starts with understanding your current tax position and identifying opportunities.

Your Roadmap: From Tax Frustration to Tax Confidence

You know you’re overpaying. You’ve felt it every April. You’ve heard stories of other business owners keeping more of what they earn, and you wonder why that isn’t you.

It doesn’t have to be this way.

Moving from tax frustration to tax confidence requires three commitments:

Commit to year-round advisory. Swap your annual tax appointment for quarterly planning conversations. This is the foundational shift that makes everything else possible.

Commit to transparency. Share your business plans, revenue trajectory, expense timing, and financial goals with your tax advisor. The more context we have, the more precisely we can optimize your situation.

Commit to action. Proactive planning surfaces opportunities. But opportunities only create value when they’re executed. We’ll recommend strategies backed by documentation and legal standing. You implement them knowing they’re sound.

These three commitments transform your relationship with taxes. You move from passive frustration to active management. You move from April surprises to October confidence.

The clock is already ticking on 2026. If you’re serious about keeping more of what you earn, this is the moment to start. Not after tax season. Now.

We specialize in serving service-based business owners exactly like you: those with $2M+ in revenue and $500K+ in taxable income who are tired of overpaying and ready for a proactive alternative. We’ve designed our entire approach around your complexity.

Schedule a conversation with us. We’ll analyze your current situation, identify opportunities, and show you exactly what’s possible. No guessing. No generic advice. Just a clear roadmap from where you are to where you should be.

Your tax dollars deserve better than a once-a-year conversation with an accountant who’s reviewing history. They deserve a strategist who’s designing your future.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Recent Comments