Table of Contents

- The Problem: Missing Six-Figure Tax Savings Right in Front of You

- Why Most Service Business Owners Leave Money on the Table

- How Section 179 Works: Immediate Deductions Instead of Long-Term Depreciation

- Bonus Depreciation: The Accelerated Path to Tax Savings

- Combining Section 179 and Bonus Depreciation: Our Strategic Approach

- Real-World Examples: What Service Businesses Actually Save

- Common Mistakes That Cost You Deductions

- The Material Participation Rule: Staying Audit-Proof

- Building Your Equipment Strategy into Annual Tax Planning

- How We Help You Maximize These Deductions Year After Year

- Your Next Move: From Strategy to Implementation

- Frequently Asked Questions (FAQ)

The Problem: Missing Six-Figure Tax Savings Right in Front of You

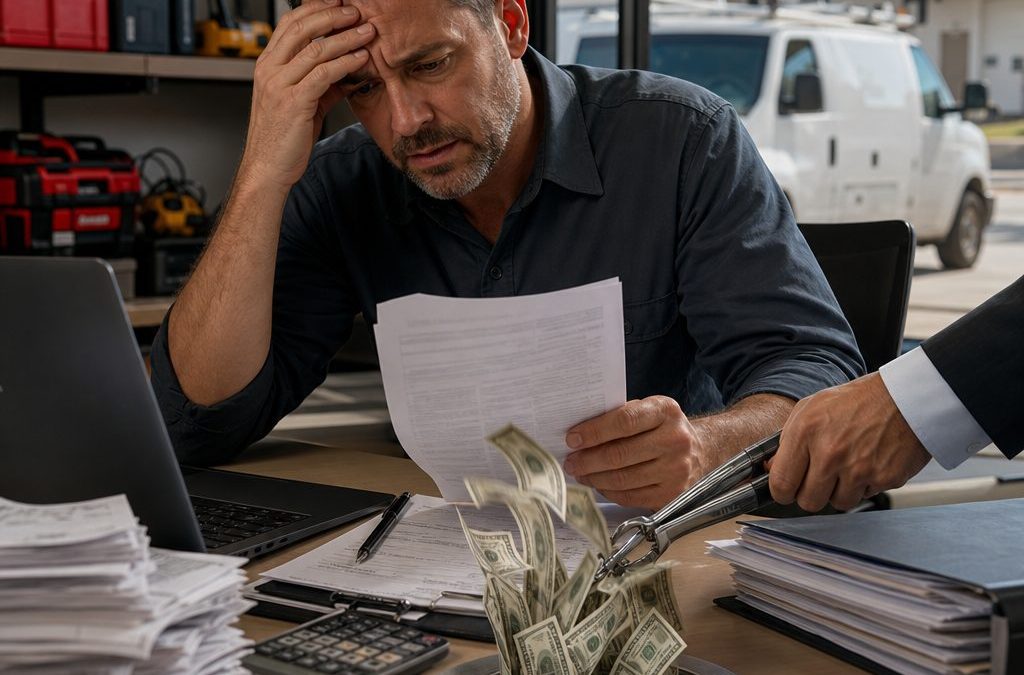

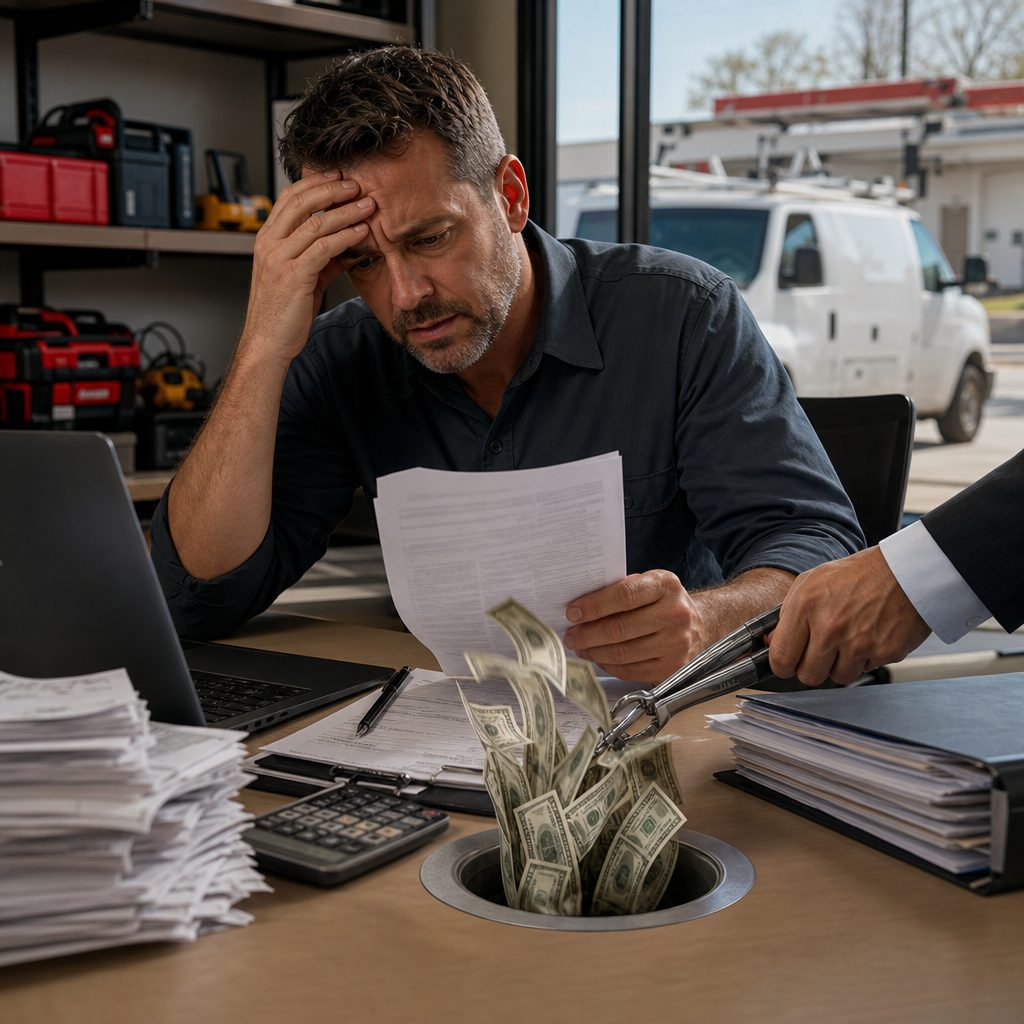

You’re making solid money. Your service business pulls in $2M plus. But when tax season rolls around, you’re shocked by what Uncle Sam wants. Many service business owners with significant income feel this sting: the bulk of their earnings gets taxed as ordinary income at the highest federal rate (37% for 2026).

Here’s what most don’t realize: you have legitimate tools sitting unused that can defer or eliminate six figures in taxable income. Section 179 and bonus depreciation aren’t exotic loopholes. They’re standard tax code provisions designed specifically for business owners who invest in equipment and assets.

The gap between what you’re paying now and what you could legally owe is often $50,000 to $300,000 or more per year. That’s not theoretical. That’s the difference between keeping what you’ve earned and handing it over to the IRS.

Actionable takeaway: Before you file your next return, audit what equipment and assets your business actually owns. You may already have deductions you’ve never claimed.

Why Most Service Business Owners Leave Money on the Table

Service businesses operate differently than manufacturing or retail. You sell expertise, labor, and relationships. Your overhead is often lean. But here’s where most miss the boat: they underestimate the equipment they actually deploy.

Think about what your business uses daily:

- IT infrastructure (servers, software, workstations, security systems)

- Vehicles and fleet management tools

- Office furniture and fixtures

- Software licenses and digital platforms

- Diagnostic or testing equipment

- Specialized tools and machinery

- Security, HVAC, and building improvements

Many service owners treat these as operating expenses rather than depreciable assets. Others buy equipment but never document it properly for tax purposes. Some assume small purchases can’t matter. And a troubling number work with advisors who default to basic depreciation schedules without exploring accelerated deduction strategies.

The real culprit: lack of coordination between your bookkeeper, your accountant, and your tax strategist. When those three don’t talk, you leave money on the table. We see it constantly.

Actionable takeaway: Schedule a conversation with your tax professional specifically about equipment purchases from the last three years. Many business owners discover $20,000 to $100,000 in missed deductions just by pulling purchase records.

How Section 179 Works: Immediate Deductions Instead of Long-Term Depreciation

Section 179 is your fast-track tool. Normally, when you buy equipment, you depreciate it over 5, 7, or even 39 years depending on asset class. Section 179 lets you do something radically different: deduct the full purchase price in the year you place it in service.

Here’s the mechanics. You buy a $50,000 diagnostic system in January. Under normal depreciation, you’d write off roughly $7,000 per year for seven years. Under Section 179, you deduct the full $50,000 in year one, reducing your taxable income by $50,000.

For 2026, the Section 179 limit sits at approximately $1,365,000. That means you can immediately deduct up to $1.365M in qualifying property in a single tax year.

There are constraints:

- You must use the property in an active trade or business (material participation matters here, which we cover below).

- The property must be tangible personal property (equipment, machinery, vehicles, software, improvements to buildings in certain cases).

- You can’t claim Section 179 on property you inherit or acquire from a related party.

- Total Section 179 deductions cannot exceed your business income for the year.

The strategic power here is timing. If you know a strong revenue year is coming, you can front-load equipment purchases to offset that income in the same tax year.

Actionable takeaway: If you’re planning equipment upgrades, accelerate purchases into high-income years. Work backward from your projected taxable income to determine the optimal deduction strategy.

Bonus Depreciation: The Accelerated Path to Tax Savings

Bonus depreciation works in parallel with Section 179 and often provides even more flexibility. For qualified property placed in service in 2026, you can claim 60% bonus depreciation (phasing down in future years).

The difference: bonus depreciation applies automatically. You don’t elect it on a form like you do with Section 179. It kicks in without action if the asset qualifies.

What qualifies for bonus depreciation?

- Machinery and equipment purchased new

- Vehicles and transportation equipment

- Software (including capitalized software)

- Leasehold improvements (with limitations)

What doesn’t:

- Property subject to a depreciation election to opt out

- Property held or used before 2026 (must be placed in service for the first time in 2026 to get 100% bonus; used property has restrictions)

- Land and land improvements

- Buildings (though certain improvements qualify)

The 60% rate in 2026 means on a $100,000 equipment purchase, you get a $60,000 deduction automatically in year one. The remaining $40,000 depreciates normally (or you can apply Section 179 to that remainder, stacking the benefits).

Stacking is the secret. Many service business owners don’t understand they can layer Section 179 and bonus depreciation together on the same purchase.

Actionable takeaway: If you purchase over $1.365M in equipment in a single year, use Section 179 to max out that limit, then let bonus depreciation cover the excess. This creates six-figure deductions in high-income years.

Combining Section 179 and Bonus Depreciation: Our Strategic Approach

We don’t choose one or the other. We architect a multi-year equipment and acquisition strategy that uses both tools in concert with your income forecast.

Here’s how we think about it:

Year 1 (High Income Year): Project your taxable income. If you’ll owe $200,000 in federal income tax, we work backward. We identify equipment purchases that, when accelerated through Section 179 and bonus depreciation, offset $200,000 of that income. You reduce your tax burden from $200,000 down to near zero (or a small amount) while upgrading your operational capability.

Year 2 (Moderate Income Year): If you don’t have excess income to shelter, you may hold off on Section 179 elections and instead use straight-line or bonus depreciation, which reduces taxable income more gradually.

Years 3-5 (Planning Ahead): We track what you’ve already deducted. If you’ve used Section 179 aggressively in year one, we plan whether to repeat the strategy or shift to bonus depreciation and normal cost recovery.

The framework we use:

- Audit your balance sheet for assets not yet depreciated

- Project next three years of business income

- Identify equipment needs and upgrade cycles

- Model Section 179 elections and bonus depreciation claims

- Time purchases to align with income peaks

- Document material participation to protect deductions

This coordination is why most service businesses working with generalist accountants miss the savings. They don’t build a [proactive tax reduction strategy] that pulls these levers together. We do it systematically.

Actionable takeaway: Don’t make equipment decisions in isolation. Build them into a 3-year tax plan. Work with your CPA to model how each purchase reduces your specific tax liability.

Real-World Examples: What Service Businesses Actually Save

Let’s pull back the curtain with concrete numbers.

Consulting firm: $3M revenue, $800K taxable income

This eight-person firm needed to upgrade IT infrastructure and add a project management platform. Total cost: $85,000 over Q1 and Q2. Under normal depreciation, the tax benefit would’ve trickled in over five to seven years. We elected Section 179 on $85,000, reducing taxable income from $800,000 to $715,000. Tax savings: approximately $29,750 (at combined federal and state rates). Year-one cash flow impact: positive. The business kept nearly $30,000 it would’ve paid in taxes while making necessary infrastructure investments.

Medical billing services: $2.2M revenue, $650K taxable income

This owner bought software licenses ($120,000), office buildout ($45,000), and equipment ($35,000) totaling $200,000. Normal depreciation strategy: spread over multiple years, minimal first-year tax benefit. Our approach: combined Section 179 ($135,000 limit that year) plus bonus depreciation on the remainder. First-year tax deduction: $200,000. Tax savings: approximately $70,000. The business essentially paid for equipment upgrades with pre-tax dollars.

Engineering services: $4.2M revenue, $1.1M taxable income

Higher revenue meant higher tax bill. We identified $1.365M in equipment qualifying for Section 179 (software, workstations, testing equipment, fleet vehicles). Combined with bonus depreciation on items exceeding that ceiling, we reduced taxable income by $1.8M. Tax savings: approximately $630,000 (federal and state blended rate). Results mentioned are not typical and individual results will vary based on your specific situation.

These aren’t fantasy numbers. These are outcomes from service businesses we’ve worked with. They bought equipment they needed anyway and structured the deductions strategically.

Actionable takeaway: Calculate what a $100,000 equipment purchase saves you in taxes at your marginal rate. If you’re in the 37% federal bracket plus state taxes, that’s $40,000+ in savings. That’s a 40% return before depreciation benefits even matter.

Common Mistakes That Cost You Deductions

We see the same errors repeatedly. Avoid these or lose five figures.

Mistake 1: Not documenting the purchase and placement date properly

Section 179 requires the asset be “placed in service” in the tax year you claim it. If you buy equipment in December but don’t set it up until February of the next year, you can’t deduct it in year one. We track dates obsessively. You should too.

Mistake 2: Mixing personal and business use without apportionment

You buy a $40,000 truck. Your business uses it 60% of the time; you use it personally 40%. You can only deduct 60%. If you claim 100%, the IRS will disallow it and add penalties. Document business-use percentage from day one.

Mistake 3: Failing to elect Section 179 on time

Section 179 is elected on your tax return (Form 4562). If your return is filed without the election, you miss it. Extensions give you some breathing room, but you can’t amend a return filed two years ago and suddenly claim Section 179. File on time. Coordinate with your CPA by October if you file extensions.

Mistake 4: Buying “used” property and missing bonus depreciation restrictions

Used property has different rules. For 2026, used tangible property generally doesn’t qualify for 100% bonus depreciation unless specific conditions are met. If you buy used equipment, verify its status. Buying new often makes more tax sense than buying used even if the used price is lower.

Mistake 5: Ignoring the income limitation

Section 179 deductions can’t exceed your business taxable income. If your business makes $300,000 and you claim $400,000 in Section 179, the IRS disallows the excess. It carryforwards, but you need income to absorb it. Know your income projection before committing to Section 179 elections.

Mistake 6: Treating leasehold improvements as non-depreciable

Many service businesses lease office space. Improvements you make (flooring, walls, fixtures) are depreciable. Some owners wrongly assume they can’t deduct improvements to leased property. You can, and they can qualify for Section 179 and bonus depreciation under current rules.

Actionable takeaway: Before claiming any equipment deduction, verify three things: (1) placement date, (2) business-use percentage, (3) your projected business income. Get one wrong and the entire deduction may vanish.

The Material Participation Rule: Staying Audit-Proof

This is where we protect you legally. Equipment deductions are only valid if you materially participate in the business. For service businesses, this usually isn’t an issue. You’re out delivering services, managing projects, meeting clients. That’s material participation.

But here’s the nuance: if you’re passive (silent investor, limited partner, absent owner), your ability to claim equipment deductions changes. Passive activity loss rules can limit or defer deductions.

The IRS uses a “100-Hour Test”: if you participate in the business at least 100 hours during the year and no one else participates more than you, you’re materially participating. For service businesses with owner involvement, you hit 100 hours easily. One month of client work often gets you there.

Red flags that invite IRS scrutiny:

- Owner is barely involved (less than 100 hours annually)

- Equipment is purchased through a pass-through entity but business income is limited

- Large Section 179 elections in years with low business income

- Equipment doesn’t logically relate to the services offered

If you’re buying a $200,000 diagnostic device for an accounting firm and the firm nets $50,000, that mismatch gets attention. We align equipment purchases with your business scope and income level to stay audit-proof.

Always consult with a qualified tax professional before implementing any tax strategy. We ensure every deduction we recommend sits cleanly within IRS guidelines and is well-documented.

Actionable takeaway: Document your involvement in the business. Keep a log of hours worked and projects managed. If audited, this proves material participation and protects your deductions.

Building Your Equipment Strategy into Annual Tax Planning

Equipment decisions shouldn’t happen in June when you find extra cash or in December as an afterthought. We build them into your annual tax plan starting in Q3.

Here’s our process:

Q3 Planning: We project your year-end income. If trends show a strong year, we identify equipment needs and budget capital purchases.

Q4 Strategy: We model different scenarios. What if you buy $200,000 in equipment? $400,000? We show you the tax impact of each. You decide based on business need and tax savings.

Execution: Once you commit, we ensure purchases happen with proper documentation. We track placement dates and business use carefully.

Tax Return Prep: When it’s time to file, we have all Section 179 elections prepared and ready. No surprises. No missed deadlines.

Q1 Following Year: We review what was claimed and adjust projections for the next year. Did deductions hit as expected? Do we need to adjust strategy?

This systematic approach turns equipment acquisition from a tax hassle into a strategic advantage. You buy what you need. We optimize the tax outcome.

Actionable takeaway: Schedule a Q3 planning call with your tax advisor. Discuss next year’s capital needs now, not in December.

How We Help You Maximize These Deductions Year After Year

We don’t do one-off tax returns. We partner with service business owners for multi-year tax reduction.

Here’s what partnership looks like:

We start with a deep dive into your balance sheet, equipment inventory, and historical deductions. We identify missed opportunities from prior years. In some cases, we file amended returns to recover Section 179 deductions you never claimed.

We then build a three-year equipment and tax strategy aligned with your business goals. If you’re planning to hire staff, we factor in equipment needs for that expansion. If you’re investing in new service lines, we time capital purchases to offset the income those lines generate.

Throughout the year, we stay connected. You share major purchase plans with us. We advise whether to time them differently or structure them for maximum benefit. We ensure material participation is documented. We review Q3 projections and adjust strategy if needed.

When tax time arrives, your return is built on a strategy, not just last-minute optimization. You’re not guessing. You know exactly what deductions are coming and why they’re defensible.

We’ve helped service business owners like you [keep more of what you earn] by systematically unlocking depreciation and Section 179 benefits. Many clients save $50,000 to $200,000 annually through this coordinated approach.

This information is for educational purposes only and does not constitute tax, legal, or financial advice.

Actionable takeaway: If you’ve never had a dedicated tax strategist model your equipment and depreciation strategy, that’s your next step. The gap between what you’re paying and what you should owe is likely six figures.

Your Next Move: From Strategy to Implementation

You now understand Section 179, bonus depreciation, and how to stack them for maximum benefit. You’ve seen real examples of service businesses saving tens of thousands annually.

The gap between understanding and action is where most business owners get stuck. They read this, nod, and do nothing.

Don’t be that owner.

Start here:

- Audit your last three years of tax returns. Did you claim Section 179? Did your CPA mention bonus depreciation? If not, you likely left money on the table.

- Pull your equipment inventory. List every business asset: vehicles, software, hardware, tools, improvements, furniture. Note purchase dates and cost.

- Project your next two years of income. Work with your accountant or bookkeeper to forecast taxable income. That forecast drives your equipment strategy.

- Schedule a tax strategy call. Bring your equipment list and income projection. A qualified tax professional can model the deductions and show your potential savings.

- Document material participation. Start logging hours and project involvement now. This protects your deductions.

The business owners we work with didn’t get ahead by accident. They got ahead by being intentional about tax strategy. They didn’t leave six figures on the table. They kept it.

You can do the same. The tools exist. The strategy is proven. The only question is whether you’ll implement it.

Let’s talk about your specific situation. Reach out to us at Ed Lloyd & Associates when you’re ready to move from reading about tax reduction to actually executing it. We turn equipment purchases and depreciation strategy into real tax savings year after year.

Your next move is simple: stop letting the IRS take more than they’re owed.

For further reading: Strategic advisory for service businesses.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

What’s the difference between Section 179 and bonus depreciation, and which one should we use?

Section 179 lets us deduct the full cost of qualifying equipment in the year we purchase it, up to annual limits ($1,160,000 in 2026). Bonus depreciation allows us to immediately write off a percentage of the equipment’s basis without hitting Section 179 caps. We typically layer both strategies together: we use Section 179 for our most impactful purchases and bonus depreciation to capture additional deductions on remaining equipment. The right combination depends on our specific income situation and purchase timeline, which is why we build this into our annual tax planning.

Can we really save hundreds of thousands using these depreciation strategies?

Yes, but results depend entirely on our equipment purchases, revenue level, and taxable income structure. A service business generating $3M in revenue with $800K in taxable income that strategically purchases $500K in equipment could legitimately reduce taxable income by that full amount through accelerated depreciation. However, we must maintain material participation in the business and follow IRS rules precisely to avoid audit risk. Results mentioned are not typical and individual results will vary based on your specific situation.

What happens if we misuse Section 179 or bonus depreciation and trigger an audit?

We work with you to ensure every deduction we claim is defensible and supported by documentation. The most common audit triggers are claiming deductions on non-qualifying property or failing to meet material participation requirements. This is why we handle the strategy, documentation, and filing coordination together rather than leaving it to chance. Always consult with a qualified tax professional before implementing any tax strategy.

Recent Comments