Table of Contents

- The Hidden Costs of a Messy CPA Transition

- Why Most Business Owners Dread Changing Accountants

- How Disorganized Bookkeeping Derails Your Tax Strategy

- The Right Way to Structure Your Records for a Smooth Handoff

- What to Demand From Your Current CPA Before You Leave

- Building a Bookkeeping Foundation That Works With Any Accountant

- How We Handle CPA Transitions for Our Clients

- Red Flags That Signal It's Time to Switch

- Creating a Transition Checklist That Protects Your Tax Position

- The Strategic Advantage of Clean, Organized Financial Records

- Frequently Asked Questions (FAQ)

The Hidden Costs of a Messy CPA Transition

Switching CPAs feels safer when you assume “the records will just transfer over.” That assumption costs most service business owners thousands in lost tax optimization and accounting chaos.

A messy transition typically creates three expensive problems. First, your new CPA inherits incomplete or poorly organized bookkeeping and spends weeks reconstructing your financial story instead of strategizing your taxes. Second, critical tax planning opportunities from prior years get missed because nobody clearly documented the logic behind your accounting choices. Third, you lose continuity in how your business structure, deductions, and entity strategy have evolved.

We’ve worked with dozens of business owners who switched firms poorly. The pattern is consistent: they paid their old CPA, paid their new CPA for cleanup work, and still ended up filing returns that didn’t capture available strategies. The real cost wasn’t the transition fee. It was the missed tax reduction that they’ll never recover.

Your next move: Request a clear handoff plan from your current CPA before you commit to leaving. If they resist transparency or demand unreasonable fees for document transfer, that’s a red flag worth noting.

Why Most Business Owners Dread Changing Accountants

Fear of transition ranks right up there with fear of the IRS for business owners. You’ve built a working relationship, shared confidential financial details, and grown accustomed to how they do things. Walking away feels risky.

The real anxiety, though, stems from legitimate concerns. What if the new firm discovers your old CPA missed deductions? What if your records are scattered across multiple platforms and nobody knows what’s actually been reconciled? What if you’re liable for errors that nobody catches until audit time?

Here’s the truth we tell clients: Most transitions go fine when you’re intentional about the handoff. Most transitions go sideways when you assume it’ll happen naturally or when your old CPA doesn’t cooperate fully.

The emotional weight matters. You’re not just changing service providers. You’re moving years of financial history and operational context. That’s worth taking seriously, but not worth staying with an accountant who isn’t aggressively reducing your taxes.

Your action: Separate the emotional attachment from the financial decision. Ask yourself this: “Is my CPA proactively identifying tax reduction strategies, or are they just filing my return each year?” If it’s the latter, a transition is overdue.

How Disorganized Bookkeeping Derails Your Tax Strategy

Poor bookkeeping isn’t just sloppy. It actively kills your ability to reduce taxes.

Consider this scenario: You operate a service business with $3M in revenue and $600K in taxable income. Your bookkeeper threw expenses into broad categories without supporting documentation. Your old CPA took a conservative approach and claimed only the obvious deductions. A new CPA arrives and wants to implement a solid tax strategy, but they can’t verify which expenses are actually legitimate because the trail is cold.

That’s when they tell you, “We can’t support those deductions in an audit. Let’s stick with what your last firm claimed.”

Bad bookkeeping creates audit liability. It also narrows your strategic options. Tax strategies like cost segregation, bonus depreciation, and loss optimization require clean, well-documented foundations. If your bookkeeper recorded equipment purchases as office supplies, a strategy that should save you $50K becomes impossible to defend.

When you switch CPAs, disorganized records become ammunition against you. Your new firm has to either spend billable hours fixing the foundation, or they file conservative returns that miss opportunities.

The fix starts before you switch. Demand that your current bookkeeper or accountant provide a detailed chart of accounts, account reconciliations, and a clear methodology for how major expense categories were categorized. If they can’t explain it, you have a problem.

Your immediate step: Pull your last three years of bookkeeping records and ask yourself: Could a stranger understand how these were organized? If the answer is no, fix it now while you still have your current CPA available to explain their reasoning.

The Right Way to Structure Your Records for a Smooth Handoff

Clean records follow a simple principle: Every transaction should tell a story that a third party can follow.

This means your chart of accounts needs to be logical and consistent. Don’t bury travel expenses under “miscellaneous” or split auto expenses across four different accounts because someone felt creative one month. Use a standard structure like this:

- Income (organized by revenue stream if applicable)

- Cost of Goods Sold or Cost of Services (direct expenses tied to revenue generation)

- Payroll and Related Expenses (wages, taxes, benefits)

- Office and Administrative (rent, utilities, supplies, insurance)

- Travel and Meals

- Professional Services (accounting, legal, consulting)

- Depreciation and Amortization

- Other Operating Expenses

Each month’s reconciliation should be complete. Your bank account, credit card accounts, and loan balances should reconcile to your general ledger. If they don’t, the gap signals missing transactions or errors that compound confusion during a transition.

Supporting documentation matters too. Keep receipts, invoices, and payment records organized by date and category. When your new CPA asks, “Why is this $8K charge in travel?” you should be able to point to a document that proves it.

For businesses with multiple bank accounts, credit cards, or complex structures, document the purpose of each account. Don’t leave a new CPA guessing why you have three business bank accounts.

Your next action: Spend a weekend organizing your current year’s records into this structure. If it takes more than a few hours, your bookkeeping system needs a serious upgrade before you switch firms.

What to Demand From Your Current CPA Before You Leave

Your current CPA has a responsibility to facilitate a clean transition, even if they’re disappointed you’re leaving. Here’s what you must insist on:

- A complete copy of all work papers, tax returns (last three years minimum), and financial statements in both digital and paper form

- A written memo documenting all accounting methods, entity elections, and tax positions they’ve taken on your behalf

- Access to all software accounts (accounting platform login, tax software, any planning tools they used)

- A detailed list of all estimated tax payments, extensions filed, and any pending IRS correspondence

- Written confirmation that they’ve provided complete information and disclaimed responsibility for any issues discovered after transition

Don’t settle for vague promises. Get it in writing. If your CPA resists any of these requests, that’s a sign they weren’t running a transparent operation.

Many firms will ask for a transition fee or refuse to release documents until you settle your account. That’s standard and reasonable. Pay what you owe promptly. But demand complete documentation in exchange.

Red flag: If your CPA demands payment of future-year returns before releasing current records, or if they claim “we own the work product,” walk away. That’s not how legitimate accounting practices operate.

Your move: Send a professional email requesting these items specifically. Keep records of what you asked for and what you received. This protects you if questions surface later.

Building a Bookkeeping Foundation That Works With Any Accountant

The goal isn’t to find a CPA who fits your current bookkeeping system. It’s to build bookkeeping that any competent CPA can work with.

This means choosing a platform that’s widely used and transferable. QuickBooks Online, Xero, and similar cloud-based solutions are industry standards. Your bookkeeper can switch between CPAs easily because the data exports cleanly. Excel spreadsheets or proprietary systems created by your current accountant are poison. They lock you in and create friction during transition.

Monthly reconciliation is non-negotiable. If your bookkeeper isn’t reconciling your bank accounts to your general ledger every month, you’re flying blind. Reconciliation catches errors early, before they compound into a mess.

Clear naming conventions help too. “Truck Repair” is clear. “Misc Maintenance” is ambiguous. “Meals 1-15-26 Client Meeting” is specific and auditable.

For businesses with multiple revenue streams, expense allocations, or investments in equipment and real estate, a written accounting procedures manual is worth gold. It documents decisions so the next CPA doesn’t have to guess why you recorded something a certain way.

When you’re ready to switch CPAs, having this foundation in place cuts your transition time by weeks. Your new firm can jump straight into strategy instead of debugging bookkeeping.

Your action today: Evaluate your current bookkeeping platform. If it’s not exportable or cloud-based, schedule a conversion before you make any other changes.

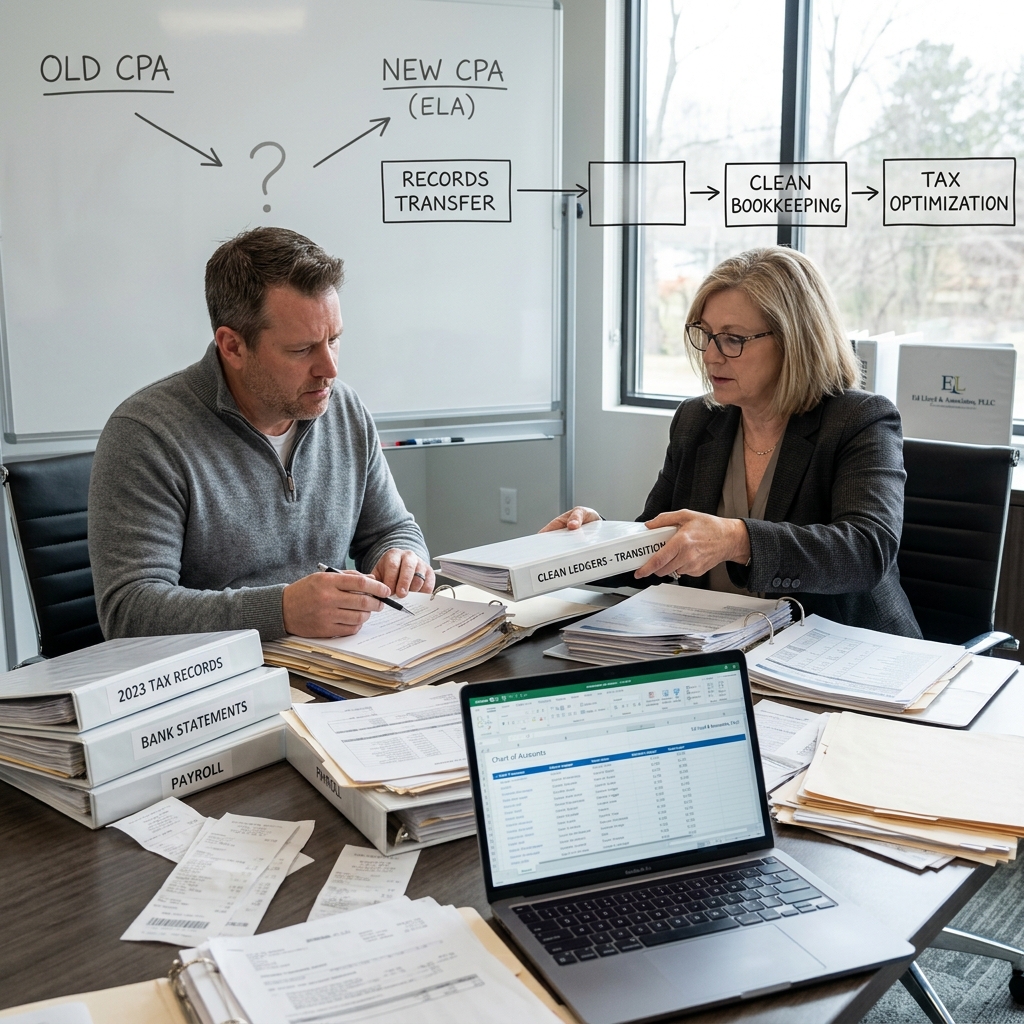

How We Handle CPA Transitions for Our Clients

We’ve engineered our transition process specifically for service business owners who want zero friction when moving from their old firm.

Here’s the framework we use. First, we request a complete handoff from your previous CPA in writing. We also conduct an initial audit of your last three years of returns and bookkeeping to identify any missed strategies or potential audit exposure. We then document all prior positions and create a memo explaining what we’re keeping, what we’re changing, and why.

Second, we reconstruct your financial story year by year. We look at major transactions, entity structure decisions, and prior-year tax positions. We ask detailed questions about your business operations, income timing, and any investments you’ve made. This takes time, but it prevents surprises.

Third, we map opportunities specific to your situation. For high-income service business owners, we look for strategies around entity structure, loss conversion, cost segregation, and income timing that your prior CPA may have missed.

Finally, we build a clean, documented foundation going forward. We align your bookkeeping with our planning, we schedule quarterly check-ins so surprises don’t build up, and we communicate proactively about tax positions we’re taking on your behalf.

Because we specialize in reducing income taxes for service business owners with $2M+ in revenue and $500K+ in taxable income, we know which structures and strategies apply to your situation. We pull back the curtain on how taxes work and show you exactly what strategies we’re using to help you keep more of what you earn.

This approach takes more work upfront than a passive transition. But it’s the only way to ensure you’re not leaving money on the table.

Contact us to discuss your specific situation and learn whether a transition makes sense for your business.

Red Flags That Signal It’s Time to Switch

You should switch CPAs if any of these patterns describe your current relationship:

Your CPA files your return without a detailed planning conversation. If they hand you a bill and a return with zero explanation of strategy or opportunity, they’re not earning their fee.

They’re unavailable or slow to respond. Tax planning is time-sensitive. If your CPA takes weeks to answer questions, you’re losing opportunities that move fast.

They haven’t reviewed your business structure in three years. Your entity structure should evolve with your business. A CPA who doesn’t revisit this annually is leaving optimization on the table.

They file extensions every year but don’t use that time for planning. Extensions are supposed to buy time for strategy, not just convenience.

They can’t explain their recommendations in plain English. Jargon without clarity is a sign they don’t fully understand your situation.

They actively discourage questions about tax strategy. A defensive posture signals they’re not confident in their advice.

Your tax bill hasn’t changed meaningfully in years despite your revenue growing. Growth should create new planning opportunities. If your taxes stay flat while your income climbs, your CPA isn’t working.

Any of these is worth taking seriously. Combined, they suggest a transition would likely benefit you.

Creating a Transition Checklist That Protects Your Tax Position

Use this checklist to manage your transition systematically:

Before You Tell Your Current CPA You’re Leaving:

- Confirm your new CPA is willing to take your account (include full transition context)

- Gather all personal financial documents (mortgage, investments, insurance)

- Request and review your last three years of tax returns

- Pull the last 12 months of bookkeeping records

Notification and Handoff:

- Notify your current CPA in writing that you’re transitioning

- Request a specific list of documents and login credentials

- Confirm what fees will be charged for the handoff

- Set a deadline for receiving all materials (typically 10-15 business days)

With Your New CPA:

- Provide all documents from your old CPA (originals, not copies)

- Have a detailed conversation about any prior-year tax positions or strategies

- Discuss your business structure and any changes you’re considering

- Review your prior three years for missed opportunities

Going Forward:

- Confirm your new CPA has access to all accounts and software

- Establish a quarterly planning meeting schedule

- Agree on bookkeeping standards and monthly reconciliation

- Document major tax decisions in writing

Final Step:

- Keep copies of all correspondence related to the transition for your records

This structure prevents handoff gaps and gives you a clear record if questions surface later.

The Strategic Advantage of Clean, Organized Financial Records

Here’s the real payoff: Clean records unlock proactive tax strategy instead of reactive compliance.

When your bookkeeping is transparent and organized, your CPA can spot optimization opportunities that would be invisible in a messy system. They see the shape of your business clearly. They understand your cash flow, your expense patterns, and your income timing. From that clarity, strategy emerges.

A business owner with $600K in taxable income and clean records might qualify for bonus depreciation on new equipment, loss conversion opportunities if they own rental property, or timing strategies around service delivery that reduce next year’s tax bill by 20% or more. But a business owner with the same income and messy records can’t capture those opportunities because the CPA is too busy cleaning up the foundation to think strategically.

We’ve seen clients reduce their income tax by 50% or more by switching to a CPA who structures their records strategically and implements proactive planning. But that result isn’t typical, and individual results vary based on your specific situation. It requires three things: Clean records, a CPA committed to strategy, and a business owner willing to make structural or operational changes that optimize taxes.

If your current CPA treats tax preparation as a compliance event rather than a planning opportunity, a transition could unlock significant money. Not because your old CPA was bad at their job, but because they weren’t thinking about your specific situation strategically.

The transition process we’ve outlined here takes work. But it ensures you don’t lose ground during the move. You preserve continuity, you capture prior opportunities, and you build a foundation for aggressive tax optimization going forward.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

Ready to explore whether a transition makes sense for your business? We work specifically with service-based business owners earning $500K+ in taxable income who want to reduce their tax burden strategically. Reach out to discuss your situation.

For further reading: CPA Tax Reduction Services.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Frequently Asked Questions (FAQ)

What happens to my financial records when I switch to your firm?

We take full ownership of organizing and securing your transition. Our process starts by collecting your complete bookkeeping history from your previous CPA, then we audit it for gaps or errors that could cost you on your tax return. We reconstruct your records in our system to ensure continuity and identify any missed deductions or strategic opportunities your former accountant overlooked. You’ll have complete visibility into every file and transaction from day one.

How do I know if it’s actually time to leave my current CPA?

If your CPA has never mentioned tax reduction strategies, you’re getting generic tax prep instead of proactive planning, or you suspect you’re overpaying what you actually owe in taxes, those are the red flags we see constantly. We typically find that service-based business owners are leaving 50% or more in potential tax savings on the table with conventional accounting. The real question isn’t whether it’s time to switch, but whether you can afford to stay put.

What do I need to ask my current CPA before making the move?

Demand a complete digital copy of your tax returns, general ledger, bank reconciliations, and any supporting schedules for the last three years. Ask specifically what tax strategies they’ve implemented to reduce your income tax burden and request documentation proving material participation if you have any passive loss positions. This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy.

Recent Comments