Table of Contents

- The Entity Structure That's Costing You Hundreds of Thousands

- Why Most Business Owners Get This Decision Wrong

- The Three Critical Tax Levers We Pull for Entity Optimization

- How S-Corps Unlock Material Participation and Active Loss Benefits

- Strategic Entity Layering: When One Structure Isn't Enough

- The 100-Hour Test and Passive Loss Conversion Opportunities

- Real Numbers: What Entity Optimization Looks Like in Practice

- Timing Your Entity Change for Maximum Tax Efficiency

- Common Entity Mistakes That Lock You Into Overpaying Taxes

- How We Implement Your Tax-Efficient Entity Structure

- Your Next Step: Pull Back the Curtain on Your Current Structure

The Entity Structure That’s Costing You Hundreds of Thousands

Your business entity choice is one of the three highest-impact tax decisions you’ll ever make. Yet most service-based business owners make it once, usually based on gut feel or a friend’s recommendation, then never revisit it.

Here’s what we see constantly: a $3M consulting firm structured as an LLC, paying full self-employment taxes on every dollar of profit. A $2.5M professional services partnership with zero entity optimization and zero passive loss conversion. A solo S-Corp missing the opportunity to split income between W-2 wages and distributions.

The cost? Typically $50K to $300K+ annually in avoidable taxes.

This isn’t about being aggressive or bending rules. It’s about using the tax code the way Congress designed it. The same IRS regulations that apply to you apply to Fortune 500 companies. The difference is they optimize their structure. You probably haven’t.

We help service-based business owners like you unlock the playbook through strategic entity structuring. The right structure, combined with intentional business decisions, can legally reduce your income tax burden by 50% or more. Your immediate action: audit your current entity setup against the three tax levers we detail below.

Why Most Business Owners Get This Decision Wrong

Most decisions get made in a vacuum. You start your business, your accountant suggests an LLC “for liability protection,” and that’s the end of it. No one pulls back the curtain on the tax implications. No one asks: what if we layered this differently?

The mistakes cluster around three core misunderstandings:

Confusing liability protection with tax efficiency. An LLC and an S-Corp both shield your personal assets. They’re not the same tax vehicle. Choosing based only on liability is leaving money on the table.

Assuming your current situation is permanent. Your 2018 entity choice made sense when you were earning $600K. At $2.5M, the math changes completely. Most business owners never recalculate.

Underestimating the passive loss ceiling. You can’t use passive losses to offset active income under current tax law, with rare exceptions. Knowing how to convert passive losses into active losses (or trigger material participation rules) is a game-changer most owners miss entirely.

The cost of these mistakes isn’t theoretical. We’ve had clients discover they could have saved $200K+ in prior years with a simple entity restructure. That cash is gone. Your move is to fix it going forward.

The Three Critical Tax Levers We Pull for Entity Optimization

Every tax-efficient entity structure we design pulls the same three levers. This is the core playbook.

Lever 1: Self-Employment Tax Reduction. An LLC taxed as a partnership or sole proprietorship triggers 15.3% self-employment tax on all business profits. An S-Corp allows you to split income into W-2 wages (subject to payroll tax) and distributions (not subject to self-employment tax). On a $1M profit, the difference can easily exceed $40K annually.

Lever 2: Passive Loss Conversion. Rental real estate, syndications, and real estate partnerships typically generate passive losses. Under the $25K passive loss deduction rule, high earners can’t use these losses at all. Structural changes and material participation strategies can unlock these trapped losses to offset your active business income.

Lever 3: Strategic Income Splitting. Layering multiple entities, deploying family members, or using holding company structures lets you split income across multiple tax brackets. A $3M service business income shifted across three entities or two spouses changes your effective tax rate significantly.

Most business owners use zero of these levers. We deploy all three.

How S-Corps Unlock Material Participation and Active Loss Benefits

An S-Corporation is an election, not an entity type. You’re still forming an LLC or corporation, then electing S-Corp tax treatment. The magic happens in the tax code.

Here’s the core benefit: S-Corps allow reasonable salary splitting. You pay yourself a W-2 wage (subject to payroll tax at roughly 15.3%), then take the remaining profit as distributions (not subject to self-employment tax).

On $1M of business profit, you might take $400K as W-2 wages and $600K as distributions. Your self-employment tax savings alone approach $90K annually. That’s not an outlier number. That’s standard math.

The second benefit flows from material participation. When you actively participate in your business (the 100-Hour Test we detail next), you can qualify for active business status. This opens doors to convert passive real estate losses into active losses that offset your business income. For owners holding rental properties or real estate syndications, this alone can be worth six figures.

We implement S-Corp elections as a foundational move for every service-based owner earning $500K+ in taxable income. Most should have done it years ago.

Strategic Entity Layering: When One Structure Isn’t Enough

A single S-Corp is powerful. Strategic layering is transformative.

Consider a real scenario: you own an $8M consulting firm, your spouse owns a $2M marketing agency, and you both hold real estate that generates $300K in annual passive losses. One S-Corp doesn’t capture the full opportunity.

Our approach layers multiple entities:

- Operating S-Corps for each business (optimized for self-employment tax and active income)

- A holding company (often an LLC) that owns real estate and collects passive income

- Potential spousal business structures that split family income across lower tax brackets

- Real estate syndications structured as partnerships (to maximize passive loss generation)

This isn’t complexity for complexity’s sake. Each layer serves a purpose: tax bracket optimization, passive loss harvesting, liability compartmentalization, and flexibility for future business transitions.

The cost to implement is typically $3K-$8K once. The ongoing value is often $100K+ in taxes saved annually. The math is obvious.

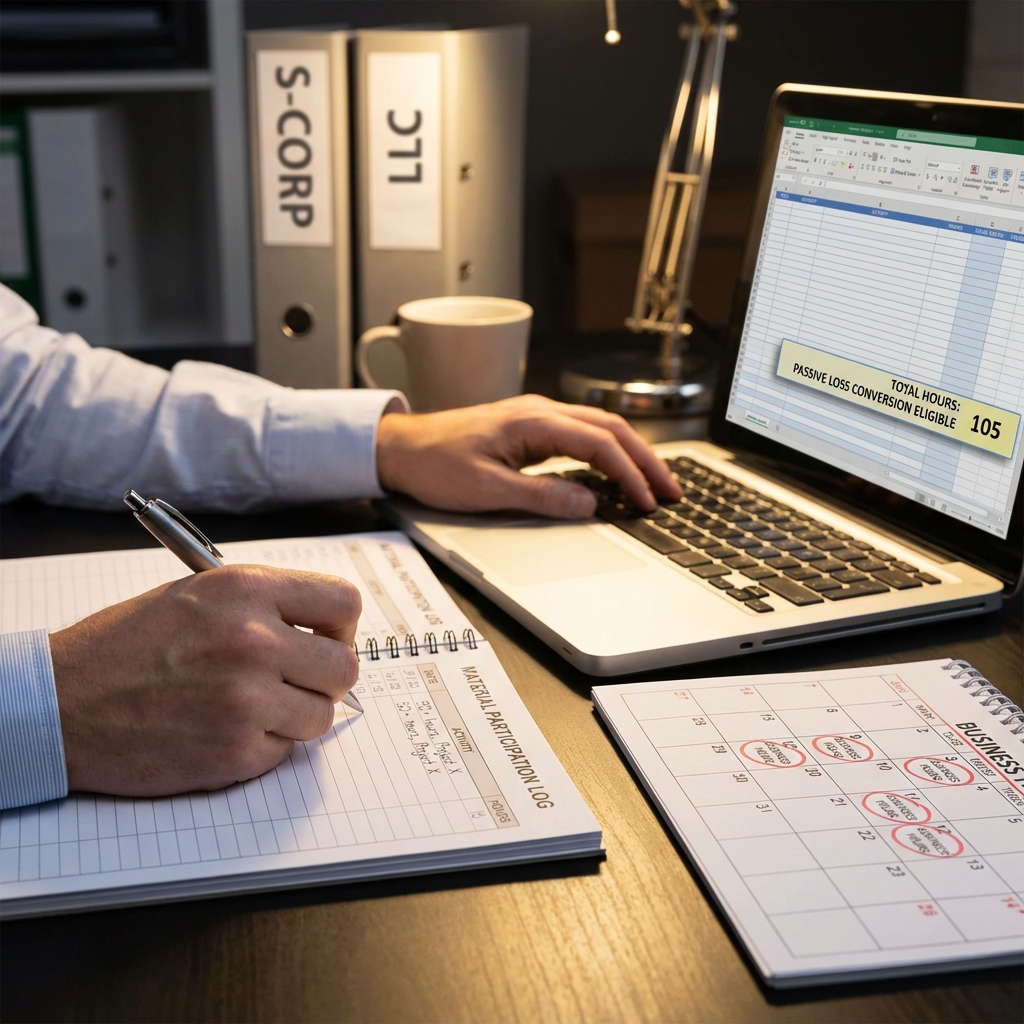

The 100-Hour Test and Passive Loss Conversion Opportunities

Material participation is a technical term with a simple meaning: you work in the business enough for the IRS to consider you an active participant.

The 100-Hour Test is one way to prove it: if you participate for more than 100 hours in a taxable year, you’re materially participating. For service business owners, this is almost always automatic. You’re running the business, not passively collecting income.

Where this gets powerful is real estate. If you own rental properties and can’t use passive losses today, proving material participation in your real estate activities (through a real estate business, active management, or partnership roles) converts those losses into active losses. Suddenly, $200K in trapped real estate losses becomes usable against your $2M consulting income.

We audit material participation status for every client. It’s one of the highest-ROI review points. Many owners discover they qualify for passive loss conversions they didn’t know existed, recovering tax benefits from prior years.

Real Numbers: What Entity Optimization Looks Like in Practice

Numbers make this concrete. Here’s a typical scenario we see:

A $3M service business owner, married, currently structured as an LLC taxed as a partnership:

- Current annual income: $1.2M in business profit

- Current tax burden: roughly $425K in combined federal, state, and self-employment taxes

- After optimization (S-Corp election + material participation + spousal income split):

– Estimated tax burden: roughly $210K – Annual savings: approximately $215K – Five-year savings: approximately $1.075M

This assumes no changes to business operations, revenue, or expenses. Just structure.

Real results vary based on your specific situation, state tax environment, spouse income, real estate holdings, and business structure decisions. But the ballpark is consistent across most of our clients earning $2M+ with $500K+ in taxable income.

We’ve also seen larger wins. A $5M operation with real estate holdings saw first-year tax savings exceed $350K through entity layering and passive loss conversion. These aren’t outliers when the initial structure is inefficient.

Timing Your Entity Change for Maximum Tax Efficiency

Entity changes mid-year create complexity, especially S-Corp elections. Timing matters.

The ideal window to make structural changes is October or November. You’re far enough through the year to model the full-year impact, but early enough in Q4 to implement before year-end.

For S-Corp elections, IRS Form 2553 has specific deadlines. Miss them and you’re locked into a taxable year with suboptimal structure. We manage these timelines obsessively.

A critical consideration: changing entities can trigger a tax event (selling assets from one entity to another, for example). Calculating the tax cost of the transition against the annual savings determines whether to move immediately or phase changes over two years.

Our analysis always runs a before/after tax projection. We show you the transition cost and the ongoing savings, then let you decide. Most owners are shocked by how quickly the transition pays for itself.

Common Entity Mistakes That Lock You Into Overpaying Taxes

We see predictable patterns in the entities that cost owners the most money:

Mistake 1: LLC without S-Corp election. An LLC taxed as a partnership is the highest-tax structure for service business owners. Simple to operate, expensive to own. Fixing this is often a one-form change.

Mistake 2: Ignoring real estate separately. Mixing real estate income with business income under one entity misses passive loss opportunities. Layering entities separates the income streams and unlocks loss conversions.

Mistake 3: Solo ownership when family income exists. Two spouses, each earning income, can structure as separate businesses. One structure often misses significant bracket optimization. This is particularly powerful when one spouse has lower active income.

Mistake 4: Keeping old entity structure from startup phase. Your 2015 entity choice made sense. Your 2026 business is likely dramatically different. Most owners never recalculate the optimization.

These aren’t judgment calls. They’re identifiable, fixable mistakes with measurable impact.

How We Implement Your Tax-Efficient Entity Structure

Our process pulls back the curtain systematically.

We start with a comprehensive entity audit: your current structure, income allocation, real estate holdings, family income, passive losses, and prior-year tax returns. We model three to five entity scenarios, showing you the tax impact of each.

Then we show you the numbers. Not theoretical benefits. Actual estimated tax liability under each structure, your savings, the transition cost, and the payback period.

Once you approve a structure, we handle the implementation. IRS forms, state filings, operating agreements, and bookkeeping changes. We coordinate with your existing CPA and manage the transition so nothing falls through the cracks.

Ongoing, we monitor your situation annually. Business growth, income changes, real estate acquisitions, and tax law shifts all affect optimization. We recalculate and adjust as needed.

This is the process we use for every service-based business owner we work with. The structure changes, but the systematic approach remains consistent.

Your Next Step: Pull Back the Curtain on Your Current Structure

You’re likely overpaying taxes through your current entity structure. The question isn’t whether optimization exists. The question is how much it’s worth to you.

Here’s what we recommend immediately: gather your last two years of tax returns, note your current business structure and income, and identify any passive losses you’re carrying forward. These three pieces of data take 15 minutes to assemble.

We offer a comprehensive entity strategy review at no charge. We’ll model your current structure against optimized alternatives, show you the estimated tax impact, and outline a concrete plan to lock in savings.

Our tax reduction services are built on this foundation. We don’t just prepare taxes. We structure your business to keep more of what you earn.

This information is for educational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified tax professional before implementing any tax strategy. Results mentioned are not typical and individual results will vary based on your specific situation.

Reach out today. Let’s show you what pulling back the curtain actually looks like for your business.

Ready to Cut Your Taxes – Schedule a game plan review and see how much you can save – https://join.elcpa.com/vsl-2

Recent Comments